China’s solar photovoltaic (PV) industry achieved another milestone in 2025, with newly installed solar capacity reaching a record 317 GWAC, representing 14 percent year-on-year growth. The expansion pushed China’s cumulative installed solar capacity to 1.2 TWAC by the end of 2025, cementing its position as the country’s second-largest power source after coal and reinforcing solar energy’s growing role in the national energy mix.

The strong deployment was supported by rising global demand for renewable energy technologies as countries accelerated their clean energy transition strategies. Despite robust installation growth, China’s solar manufacturing sector experienced a slowdown, SolarPower Europe report said.

Polysilicon production declined 27 percent year-on-year to approximately 1.34 million tons, while silicon wafer production fell 12 percent to about 680 GW. Solar cell production dropped 5 percent to around 660 GW, and module production decreased 1.2 percent to approximately 620 GW, marking declines across all four major manufacturing segments compared with 2024.

China’s long-term renewable energy strategy continues to position solar PV as the backbone of future power generation growth. Over the next five years, solar is expected to account for more than 50 percent of newly installed renewable energy capacity. By 2030, renewable power generation is projected to contribute around 30 percent of total electricity generation, supporting the national objective of increasing the share of non-fossil energy consumption to 25 percent. Looking further ahead, China aims to achieve 3,600 GWAC of combined wind and solar installed capacity by 2035.

The country is expected to maintain annual solar PV additions of more than 200 GWAC over the next decade, supporting its goals of peaking carbon emissions by 2030 and achieving carbon neutrality by 2060. Although industry forecasts suggest solar installations may decline in 2026 compared with the record levels achieved in 2025, analysts view this as a temporary adjustment rather than a structural slowdown. The anticipated moderation is largely attributed to policy-driven demand acceleration during the first half of 2025 and market-oriented electricity pricing reforms that encouraged developers to complete projects ahead of schedule.

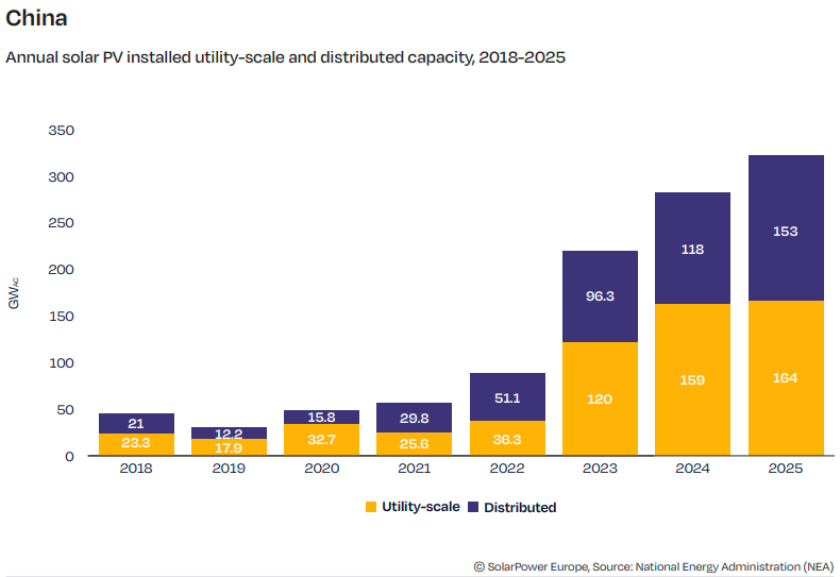

China’s utility-scale and distributed solar segments both delivered strong performances in 2025. Utility-scale installations increased 2.6 percent year-on-year to 164 GWAC, while distributed solar additions surged 30 percent to 153 GWAC. Within the distributed segment, residential solar installations climbed 56 percent to 46 GWAC, while commercial and industrial (C&I) solar projects grew 21 percent to 107 GWAC.

The transition to market-based electricity pricing has fundamentally changed the economics of solar investments in China. Revenue models are increasingly dependent on electricity price forecasting and project optimization, while energy storage is evolving from a regulatory requirement into a profitable asset. The removal of mandatory storage requirements and widening peak-to-valley electricity price differentials are creating new opportunities for flexible energy management and storage deployment.

Looking ahead to 2026-2030, China is expected to expand solar deployment through large-scale renewable energy bases in the Gobi Desert and other wasteland regions, while rooftop solar retrofitting programs for existing buildings are expected to unlock additional demand. The integration of energy storage systems and next-generation power grids is also expected to reduce grid constraints and accelerate solar adoption. According to the China Photovoltaic Industry Association, annual solar PV additions between 2026 and 2030 will remain above 200 GWAC, with 2026 installations forecast between 180 GWAC and 240 GWAC, ensuring China remains the world’s largest solar market and a key driver of the global energy transition.

BABURAJAN KIZHAKEDATH