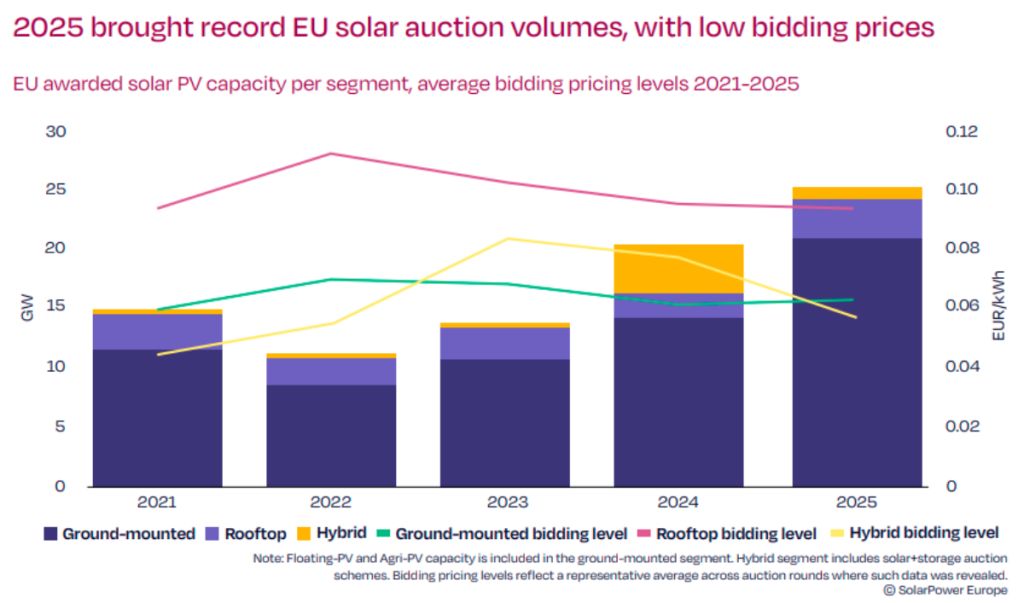

The European Union recorded a new milestone in renewable energy procurement as solar auctions and tenders awarded 25.2 GW of solar PV capacity in 2025, representing a 23 percent increase compared with 2024. The growth highlights the continued role of auctions in supporting solar expansion across Europe, even as their share in overall annual installations has fluctuated in recent years, SolarPower Europe said in a report.

Despite the record volumes awarded, auctions accounted for less than 40 percent of total solar installations in 2025, down from 52 percent in 2021. The relevance of auctions reached its lowest point in 2023, when the EU installed 63.8 GW of solar capacity, but only 22 percent came through auction mechanisms. These shifts reflect varying auction success rates, the rise and stagnation of corporate power purchase agreements (cPPAs), the increasing attractiveness of merchant solar business models, and changes in yearly solar installation volumes.

However, auctions remain a critical tool for shaping the future solar project pipeline. The significant volumes awarded in recent years are expected to support project development well beyond 2025. Since auction results secure capacity for future deployment, procurement decisions made today will continue to influence the speed and structure of solar expansion across the EU in the coming years.

Ground-Mounted Solar Dominates Auction Allocations

The ground-mounted solar segment regained momentum in 2025 after its share of awarded capacity dropped to 70 percent in 2024 due to the growth of rooftop and hybrid tenders. In 2025, ground-mounted projects captured more than 80 percent of total allocations, surpassing 20 GW in awarded capacity.

Strong participation in auctions was driven by competitive bidding. On average, submitted bid prices were around 20 percent below the ceiling support levels, providing attractive financial incentives for investors. The strong cost margin also allowed auctions to accommodate a 3 percent increase in average bid prices, largely influenced by rising capital expenditure for solar projects.

Rooftop Solar Achieves Record Auction Awards

The rooftop solar segment also reached a milestone in 2025, with 3.3 GW of capacity awarded, marking the highest level recorded for this category. While margins were narrower than those seen in ground-mounted projects, support levels for rooftop installations remained about 6 percent higher than submitted bids on average.

Several national auction schemes continue to encourage large-scale rooftop development. Programs in Italy, Germany, and France are particularly supporting commercial and industrial rooftop solar installations, contributing to the segment’s growth despite auctions traditionally focusing on large utility-scale projects.

Germany Leads Hybrid Solar and Storage Tenders

Germany remained the only EU member state to conduct hybrid renewable-plus-storage auctions in 2025 through its innovation tender program. These tenders allow combinations of wind or solar power with energy storage systems.

Although both wind and solar projects were eligible, solar paired with battery storage emerged as the dominant configuration among winning bids. The auctions attracted exceptionally strong demand, with submitted capacity exceeding offered volumes by four times.

Bidding prices in these tenders declined by 26 percent compared with the previous year, reflecting the continued drop in grid-scale battery storage costs. The program demonstrates that attractive market premiums can coexist with falling bid prices, reinforcing the economic viability and bankability of hybrid solar and storage projects.

While auctions have become an important mechanism for accelerating solar deployment in Europe, developers have faced challenges due to a volatile investment environment in recent years. Fluctuating energy prices, supply chain pressures, and changing policy frameworks have all influenced project development and bidding strategies.

The geographical distribution of solar auctions across the European Union highlights how the region’s renewable energy landscape has evolved significantly in recent years. Since 2021, more than 85 GW of solar PV capacity has been awarded through competitive auctions and tenders, making procurement programs a critical mechanism driving Europe’s solar expansion.

Germany Emerges as the Largest Solar Auction Market

Five years ago, the solar auction landscape looked very different. In 2021, the Netherlands and Poland dominated the EU solar auction market, accounting for 45 percent of total awarded capacity, followed by Germany and Italy.

However, the balance quickly shifted toward Germany, the EU’s largest solar market. Starting in 2022, Germany became the leading contributor to auctioned solar capacity and has largely maintained that position. Over the past five years, the country has awarded nearly 25 GW of solar PV capacity through tendering programs, making auctions one of the most influential policy tools supporting Germany’s rapid solar deployment.

Italy Achieves Record Solar Auction Growth

Italy’s solar auctions historically struggled due to several structural challenges, including complex permitting procedures, low remuneration levels, limited auction volumes, and frequent undersubscription. These issues limited the effectiveness of auctions as a deployment mechanism for many years.

The situation began to change in 2024 and 2025, when Italy introduced improvements to its procurement system. After allocating 2.3 GW in 2024, the newly launched FER X auction scheme delivered an impressive 10.8 GW of solar PV capacity in 2025 across ground-mounted, rooftop, and agri-PV projects.

This marked the largest single-year solar auction allocation by any EU member state, making Italy a major contributor to Europe’s solar pipeline. In total, the country has now supported around 15 GW of solar capacity through auctions, positioning it as Europe’s second largest solar auction market.

France Maintains Steady Contributions Despite Challenges

France has also played a significant role in EU solar auctions, accounting for an average of 14 percent of EU-wide awarded volumes annually since 2021. The country has supported 11.5 GW of solar capacity through auction programs so far.

Despite these contributions, France’s PPE auction framework continues to face challenges. Many auctions experience undersubscription, and recent government decisions to reduce auction volumes have slowed one of the country’s most important routes to market for solar developers.

Netherlands Transitions to New Solar Support Framework

The Netherlands ranks as the fourth largest solar auction market in Europe, awarding 10.3 GW of solar PV capacity between 2021 and 2025. However, the country has recently decided to discontinue its SDE subsidy scheme.

The government plans to replace the program with a two-way Contracts for Difference (CfD) support mechanism, aligning national policy with broader EU electricity market reforms. This shift is expected to reshape the country’s renewable procurement landscape in the coming years.

Poland Remains a Key Market Despite Lower Auction Volumes

Poland rounds out the top five solar auction markets in Europe. While the country has struggled to match its 2021 auction allocation of 3.5 GW, largely due to high undersubscription rates, the program has still played an important role in supporting renewable energy investment.

Since 2021, Poland’s auction scheme has helped deliver 7.4 GW of solar PV capacity, maintaining its importance within Europe’s auction-driven solar development pipeline.

Other EU Countries Contribute Growing Solar Capacity

Beyond the top five markets, several other EU member states have contributed to solar auction growth. Countries such as Romania, Ireland, Bulgaria, Austria, Spain, Finland, Croatia, Belgium, and Luxembourg collectively awarded 16.3 GW of solar capacity during the past five years.

Despite these contributions, the top five markets continue to dominate the EU solar auction landscape. Together, they account for more than 80 percent of all awarded solar capacity, highlighting the concentration of large-scale procurement programs in a few leading markets.

Auctions Drive a Quarter of Europe’s Solar Capacity

Overall, solar auctions have become a cornerstone of the EU’s renewable energy strategy. By the end of 2025, approximately one-quarter of the European Union’s installed solar PV capacity originated from projects supported through auction mechanisms.

BABURAJAN KIZHAKEDATH