Despite the increasing demand for power, the gas turbine market is set to face obstacles over the next 15 years due to manufacturing constraints, rising costs, and competition from renewable energy sources, Wood Mackenzie said in its report.

The report projects the addition of approximately 890 GW of new gas-fired generation capacity globally between 2025 and 2040. The United States and China are expected to account for 47 percent of global annual additions during this period, while other regions, including Southeast Asia, India, and the EU27, will collectively comprise the remaining 53 percent, Wood Mackenzie said in its report called Turbocharged vs Turbo Lag: The New Landscape for Gas-Fired Power highlights that.

However, several challenges may hinder the anticipated growth, particularly in the short term:

Manufacturing Constraints: Wood Mackenzie estimates that by 2025, gas turbine manufacturing capacity will reach 90 percent utilization. This tight capacity could delay new gas plant construction, with some US developers projecting that new combined cycle capacity may not come online until 2030 or later.

US Market Pressures: In the United States, rising capital costs and power market prices that remain below the cost of new gas generation are making new projects less viable.

Asia’s Import Costs: Despite strong power demand growth, Asia faces high imported gas costs, limiting gas to a peaking role.

European Decarbonization Goals: In Europe, ambitious decarbonization targets are pushing unabated gas to the margins by 2040.

“While natural gas-fired power will play a critical role in the energy transition through 2040, its growth potential is constrained by high fuel costs, escalating construction expenses, and continued declines in the costs of renewables and energy storage,” said David Brown, Director of Energy Transition Research at Wood Mackenzie.

Key Considerations for 2030-2040

Looking ahead, the period from 2030 to 2040 will be shaped by several critical factors:

Data Center Demand: The extent of data center demand in the US remains uncertain. Recent cancellations of major projects by tech firms have raised questions about earlier growth projections.

Manufacturing Capacity: While existing manufacturing capacity is sufficient for projected installations through 2040, manufacturers remain cautious about expanding due to past market volatility.

Net-Zero Technologies: Emerging technologies like carbon capture and storage (CCUS) and hydrogen blending present both opportunities and challenges for the gas sector.

Midstream Infrastructure: The development of midstream infrastructure will be crucial for enabling the growth of gas power.

“For the gas turbine supply chain, tight conditions in turbine deliveries are expected to persist through 2030, with potential relief in the following decade,” Brown noted.

Regional Outlook

United States: The US is expected to witness substantial growth in gas capacity driven by AI-related power demands, despite rising capital costs and power market challenges.

Europe: Renewables will dominate, but gas will remain crucial for grid stability. Germany, in particular, aims to add 20 GW of gas capacity by 2030 as it phases out coal and nuclear.

Asia-Pacific: China will lead the region in gas capacity growth, though its share will remain modest through 2040. Southeast Asia is projected to expand gas capacity rapidly, while India focuses on coal and renewables.

Latin America: The region will use gas to support renewable integration and manage peak demand, while Mexico is likely to reduce its dependence on gas as renewable capacity increases.

Potential for “Turbo Lag” (2025-2030)

Despite the anticipated expansion, the path forward is not without hurdles. Manufacturing capacity is expected to remain near full utilization in 2025, restricting additional growth and extending delivery timelines. This “turbo lag” effect could delay new combined cycle capacity in the US until after 2030.

In the US, escalating capital costs and potential trade tariffs could further elevate project costs, reaching as high as $2,800 per kW by 2028. This, combined with power market prices that often fall below the cost of new gas generation, presents a challenging investment climate.

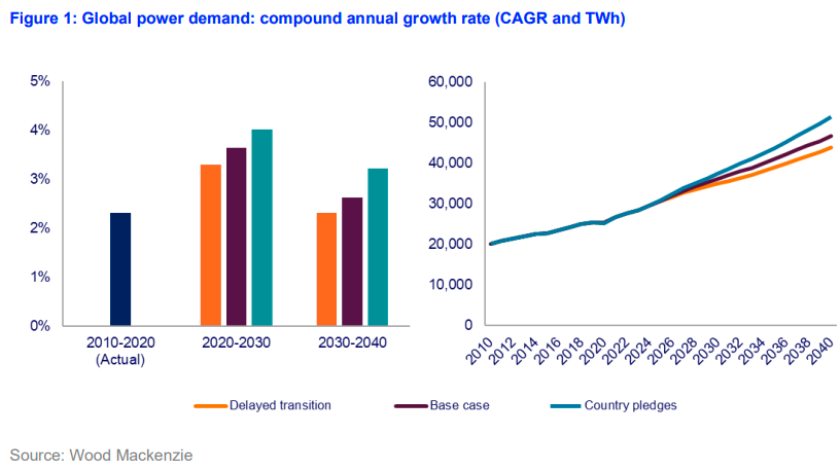

Wood Mackenzie’s base case outlook anticipates strong global power demand growth, with gas continuing to play a key role in certain markets. However, regional variations and emerging clean energy technologies will shape the future of gas-fired power in the coming decades.