At the African Energy Week event held in Cape Town, Ian Thom, Upstream Research Director at Wood Mackenzie, disclosed that the African upstream oil and gas sector is currently immersed in an ambitious $800 billion capital expenditure (capex) program. This venture is set to witness liquefied natural gas (LNG) emerge as a significant investment theme, complementing traditional deepwater oil exploration.

Thom emphasized that this 20-year investment cycle, initiated in 2010, is slated to reach its apex by the end of the decade, with the establishment of world-scale LNG projects in Mozambique and the deployment of floating LNG (FLNG) facilities across five African nations. Africa already holds a dominant position in the FLNG sector, boasting over 50 percent of global capacity and presenting prospects for additional projects to surface.

“With abundant gas resources, Africa is exploring various opportunities to develop gas for both domestic consumption and export markets,” stated Thom. He further underscored the burgeoning role of FLNG in Africa due to its adaptability, swift time to market, and suitability for handling smaller volumes. Thom projected an optimistic outlook, anticipating further expansion of FLNG projects across African resources.

West Africa Poised for LNG Growth

Thom also shed light on West Africa’s immense LNG potential, highlighting that current LNG exports from Africa stand at slightly over 40 million tonnes per annum (mmtpa). He pointed out several LNG projects in Sub-Saharan Africa (SSA) currently at different stages of development, including bp’s Tortue FLNG, strategically located offshore from Senegal and Mauritania, expected to commence operations next year.

“Tortue Phase 1 is slated to come online next year, resulting in a 2.4 mmtpa supply growth in the short term,” Thom remarked. He emphasized the favorable positioning of Senegal and Mauritania, offering easy access to European markets and significant potential in deepwater gas exploration, operating within relatively stable and supportive countries.

“Tortue Phase 1 is slated to come online next year, resulting in a 2.4 mmtpa supply growth in the short term,” Thom remarked. He emphasized the favorable positioning of Senegal and Mauritania, offering easy access to European markets and significant potential in deepwater gas exploration, operating within relatively stable and supportive countries.

Crucial Role of Mozambique LNG

Thom further highlighted the critical role of Mozambique in the future success of Africa’s LNG export aspirations. Key projects such as Coral Sul FLNG, which dispatched its maiden cargo in November 2022, along with Rovuma LNG and Mozambique LNG, were underscored as pivotal to the continent’s LNG supply ambitions. However, Thom emphasized the need for enhanced security measures in Mozambique to resume construction of onshore LNG facilities.

“Mozambique, particularly the Rovuma and Mozambique LNG projects, plays a central role in potentially doubling African LNG supply by 2035. However, there’s a risk of long-term stagnation in exports if these crucial projects fail to materialize,” Thom cautioned.

Shifting Dynamics: Gas Projects on the Rise, Oil Production Faces Challenges

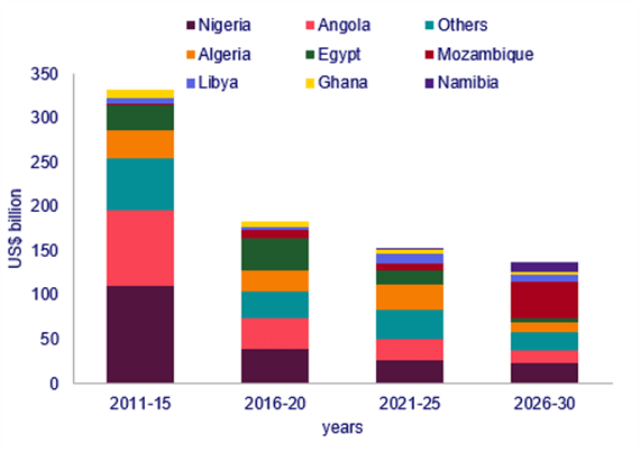

In light of the ascendant trajectory of gas projects, Thom emphasized that oil production in traditional hubs across Africa will grapple with offsetting declines at mature assets. Notably, major oil players like Nigeria, Angola, and Egypt are projected to witness oil production plateau as the decade concludes.

“With the global upstream trend firmly pivoting towards advantaged resources, oil production in higher cost and higher emitting assets in Africa will inevitably be impacted,” Thom elucidated. Nevertheless, he acknowledged potential upside from reserve growth or yet-to-find resources, citing recent discoveries like TotalEnergies’ Ntokon in Nigeria and successful exploration in Namibia as promising developments that could drive incremental growth and investment opportunities in the sector.