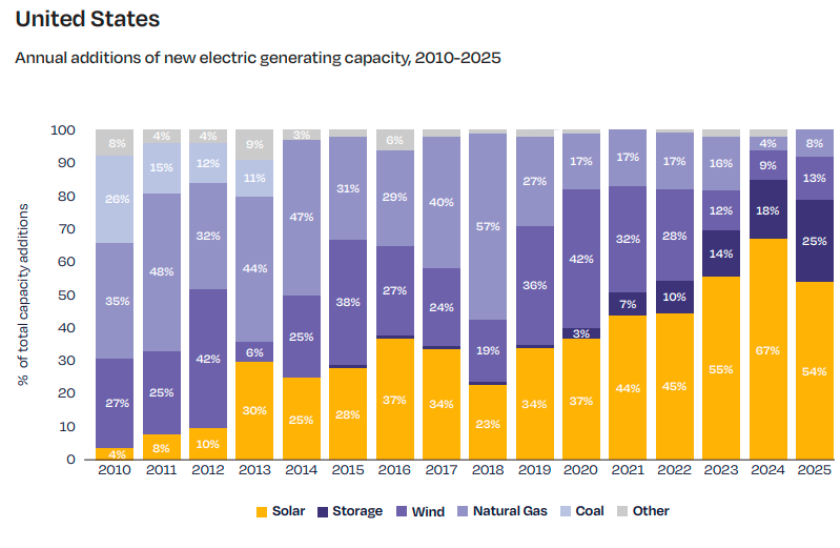

The U.S. solar industry continued to dominate new power generation capacity additions in 2025, despite policy uncertainty and regulatory changes that slowed deployment across several market segments. According to the Solar Energy Industries Association (SEIA), the United States installed 43.2 GW of new solar capacity during 2025, representing a 14 percent decline from the record 50 GW added in 2024.

Even with the slowdown, solar remained the leading source of new electricity generation, accounting for 54 percent of all new power capacity added to the U.S. grid in 2025. Combined, solar and energy storage represented 79 percent of all newly installed electricity-generating capacity, reinforcing their growing role in the country’s energy transition, SolarPower Europe report said.

The importance of solar deployment is increasing as electricity demand accelerates across the United States. Wood Mackenzie forecasts that U.S. electricity demand could grow at a 3.2 percent compound annual growth rate (CAGR) between 2026 and 2040, driven by home and business electrification, rapid expansion of data centers, and increased domestic manufacturing activity. Solar energy’s low-cost generation and fast deployment timelines position it as a critical solution for meeting rising demand without significantly increasing electricity prices.

The U.S. solar manufacturing sector also achieved major milestones in 2025. The opening of a domestic wafer manufacturing facility in the third quarter enabled the country to produce every major component of the solar supply chain locally. Nearly 70 years after the invention of the silicon solar cell, the United States now has a complete domestic solar manufacturing ecosystem. Module manufacturing capacity expanded by more than 50 percent, reaching 65.5 GW of annual production capacity, while solar cell manufacturing capacity continued to increase throughout the year.

Battery energy storage also experienced record growth. The United States recorded its largest-ever annual deployment of battery storage capacity, with installations increasing 30 percent compared with 2024, highlighting the growing integration of storage technologies alongside solar power.

However, federal policy changes created new challenges for the industry. The One Big Beautiful Bill Act (OBBB), enacted in July 2025, accelerated the phase-out of several clean energy incentives and introduced new Foreign Entities of Concern (FEOC) restrictions affecting tax credit eligibility. The Residential Clean Energy Tax Credit (25D), which allowed homeowners to deduct 30 percent of solar system costs from their taxes, expired on December 31, 2025. In addition, the Clean Energy Investment Tax Credit (48E) and Clean Energy Production Tax Credit (45Y) were assigned new deadlines, creating uncertainty for developers and manufacturers.

The impact of these policy changes was visible across multiple market segments. Utility-scale solar installations declined 16 percent compared with 2024, while the residential solar market recorded a 2 percent decline. Several gigawatts of projects originally scheduled for completion in 2025 were postponed due to regulatory uncertainty and slower permitting processes, including new federal land approval requirements.

Despite short-term challenges, the long-term outlook for U.S. solar remains strong. The country is expected to install 490 GW of additional solar capacity by 2036, increasing total cumulative installed solar capacity to nearly 770 GW. This expansion is expected to strengthen energy security, improve grid reliability, reduce electricity costs, and support America’s broader clean energy and industrial development goals.

BABURAJAN KIZHAKEDATH