The latest SolarPower Europe report has revealed what’s the size of solar PV market in Europe in terms of investment.

The report said the EU solar sector experienced a sharp slowdown in growth in 2024, with a mere 4 percent increase compared to 53 percent in 2023, marking a 92 percent decline in growth momentum.

Despite the deceleration, 65.5 GW of new solar PV was installed in 2024, surpassing the previous year’s record of 62.8 GW and bringing the EU’s operational solar capacity to 338 GW. While solar PV outperformed all other power technologies combined, the urgency for solar adoption diminished as energy bills normalized, and developers faced grid and flexibility challenges.

Between 2025 and 2028, annual growth rates are forecasted at 3-7 percent, which could be sufficient for meeting the 2030 target of 750 GW. However, in a low scenario, the EU might fall short by 100 GW. Investment trends shifted in 2024, with capital investments in solar PV dropping 13 percent to €55 billion, driven by record-low module prices and a market slowdown. Rooftop PV systems saw a minor Capex reduction of 2 percent, while ground-mounted systems experienced a sharper 28 percent decline.

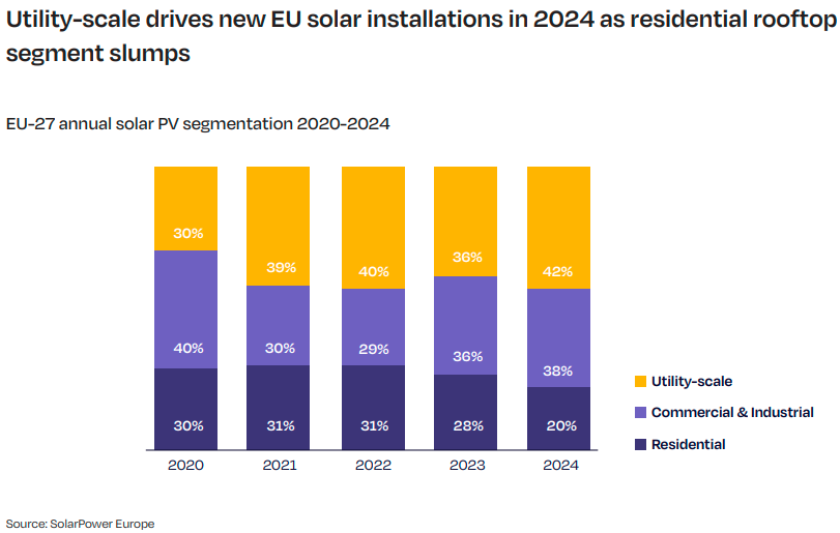

Residential rooftop solar for power demand fell significantly in 2024, with a nearly 5 GW drop to 12.8 GW, reducing its market share to 20 percent from 28 percent in 2023. Major EU markets, including Germany and Italy, contributed to this decline. However, the commercial and industrial rooftop segment grew modestly, increasing its market share to 39 percent from 36 percent. The utility-scale segment dominated the market with a 42 percent share, marking its strongest performance in five years.

The EU solar sector is experiencing a significant deceleration in growth, with capacity additions projected at 70 GW in 2025 (7 percent growth) and further slowing to 3 percent in 2026. Utility-scale projects, spurred by record-low module prices, drive short-term growth, but grid constraints and market uncertainties pose challenges.

By 2030, the Medium Scenario forecasts total solar capacity at 816 GW, exceeding the EU’s REPowerEU target of 750 GW, but this outlook reflects a downward revision of 74 GW compared to mid-2024 projections. In a Low Scenario, capacity may fall short of the target by 14 percent, reaching only 644 GW.

Solar growth has stagnated at levels similar to the previous year, highlighting the need for enhanced flexibility in the EU energy system. Despite warnings about these challenges, insufficient policy action has been taken, jeopardizing the REPowerEU targets.

To meet these goals, the EU must average 69 GW of annual installations through 2030, requiring significant progress in system flexibility and diligent implementation of EU laws. Updated National Energy and Climate Plans have improved national solar targets, yet a 59 GW gap to the REPowerEU goal persists, compounded by several Member States’ failure to submit updated plans.

Solar and inverter manufacturing in Europe is under pressure, with reductions in production capacity undermining efforts to secure a resilient supply chain. EU leaders must prioritize solar inverters for their critical role in cybersecurity and data management. Solar’s rapid and affordable deployment has been vital during the energy crisis, underscoring its importance for the EU’s energy security and competitiveness.

Battery Energy Storage Systems (BESS) must grow by 16 times, from 48 GWh in 2024 to 780 GWh by 2030, to support solar expansion. A comprehensive EU Storage Action Plan is urgently needed to address barriers like double charging, create price signals and financial incentives, and optimize battery use through service stacking. While national and EU policies include some positive measures, a more robust framework is essential to foster battery market growth and align with the EU Grids Action Plan.

Baburajan Kizhakedath