The latest International Energy Agency (IEA) analysis highlights how the ongoing conflict in the Middle East has severely disrupted global production and trade of hydrogen-based products, creating supply shortages, price volatility, and growing concerns for food security and energy diversification.

Middle East Plays Critical Role in Global Hydrogen Economy

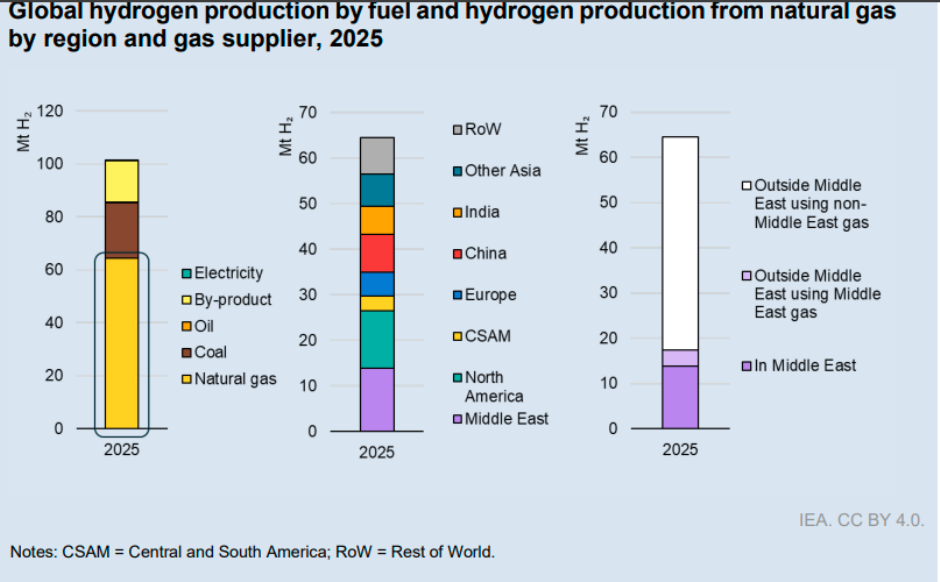

The Middle East accounts for around one-sixth of global hydrogen production, primarily supporting chemicals, fertilisers, and refined oil products. The region also represents more than 10 percent of global refining capacity, over 10 percent of global ammonia and urea production, and nearly 17 percent of global methanol production, IEA report said.

According to the IEA, several refineries and petrochemical facilities have halted operations because of supply chain disruptions, export restrictions, and direct military attacks that have damaged hydrogen production units. Recovery is expected to take weeks, while heavily damaged facilities could require months to return to pre-conflict production levels.

Global Trade Routes Severely Impacted

The disruption extends far beyond the region because the Middle East dominates international trade in hydrogen-derived products. The region accounts for more than 25 percent of global ammonia trade, almost 40 percent of global urea trade, and nearly 45 percent of global methanol trade. In addition, approximately one-third of regional refining capacity is dedicated to exports.

The closure of the Strait of Hormuz has significantly restricted shipments of ammonia, urea, methanol, refined fuels, and petrochemical products. Attacks on port infrastructure outside the Persian Gulf have further weakened export capabilities, worsening shortages across international markets.

Fertiliser Supply Chain Faces Growing Pressure

Global fertiliser markets have been among the hardest hit. Trade disruptions involving ammonia, urea, and sulphur have tightened supplies, while gas shortages and elevated natural gas prices have reduced fertiliser production in countries including Bangladesh, India, and Slovakia.

The IEA noted that approximately 25 percent of ammonia production in Bangladesh, India, and Pakistan depends on natural gas imported from the Middle East. As supply constraints intensified, urea prices doubled between January and May 2026, significantly increasing fertiliser production costs worldwide.

The impact is especially severe for import-dependent agricultural economies. Morocco imports 100 percent of its ammonia requirements, with 40 percent sourced from the Middle East. Countries including Brazil, Australia, South Africa, and Thailand rely entirely on imported urea, with 40 percent to 85 percent of supplies originating from the Middle East. The IEA warns that even modest reductions in fertiliser use could lower crop yields and create risks for global food supply chains.

Hydrogen Can Improve Energy Security, But Not Immediately

The IEA believes hydrogen and hydrogen-based fuels can strengthen long-term energy security by diversifying fuel supplies and reducing dependence on oil and gas imports. Countries can expand domestic energy production through electrolysis-based hydrogen rather than relying on gas or coal for manufacturing fertilisers, methanol, shipping fuels, and aviation fuels.

However, the agency cautions that low-emissions hydrogen is not yet available at the scale required to address immediate market disruptions. While several major projects are expected to become operational before 2030, substantial investment in production facilities, storage systems, transportation networks, and distribution infrastructure remains necessary.

Cost Challenges Continue to Slow Adoption

Policy support remains essential because low-emissions hydrogen remains more expensive than fossil-fuel-based hydrogen in most regions. China is currently the only major market where renewable hydrogen could become cost-competitive by 2030.

The IEA notes that higher fossil fuel prices can narrow the economic gap, but prolonged periods of elevated energy prices would be required to significantly improve project economics, reduce investment risks, and encourage large-scale deployment.

Global Hydrogen Demand Exceeds 100 Million Tonnes

Despite market challenges, global hydrogen demand surpassed 100 million tonnes (Mt) in 2025, driven largely by industrial and refining applications. While demand from emerging sectors is increasing, it still represents only a small portion of total hydrogen consumption.

Low-emissions hydrogen production recorded significant growth in 2025, rising 20 percent year-on-year to nearly 1 Mt. The IEA expects another record year in 2026, with low-emissions hydrogen projected to exceed 1 percent of global hydrogen production for the first time.

Current growth is being driven primarily by policy support in China and Europe, along with efforts in Japan to establish international hydrogen supply chains. However, the IEA warns that slow policy implementation, high production costs, uncertain demand, complex regulations, and inadequate infrastructure continue to limit the pace of global hydrogen adoption and prevent the sector from achieving sustainable large-scale growth.

BABURAJAN KIZHAKEDATH