The International Energy Agency in IEA’s World Energy Investment report said out of the projected $2.8 trillion global energy investment in 2023, over $1.7 trillion is expected to be directed towards clean technologies.

These clean technologies include renewables, electric vehicles, nuclear power, grids, storage, low-emissions fuels, efficiency improvements, and heat pumps. The remaining slightly over $1 trillion will be invested in coal, gas, and oil.

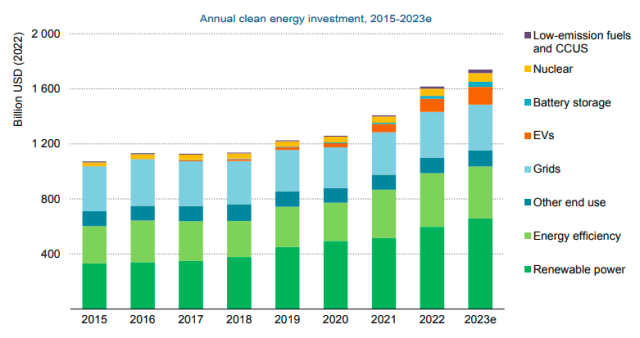

Between 2021 and 2023, annual clean energy investment is anticipated to increase by 24 percent, primarily driven by renewables and electric vehicles. In comparison, fossil fuel investment is projected to rise by 15 percent over the same period. However, more than 90 percent of this increase in clean energy investment is concentrated in advanced economies and China, which could lead to new dividing lines in global energy if other regions do not accelerate their clean energy transitions.

IEA Executive Director Fatih Birol emphasizes that clean energy is advancing at a rapid pace, with clean technologies outpacing fossil fuels in terms of investment trends. For every dollar invested in fossil fuels, approximately 1.7 dollars are now being allocated to clean energy, a notable shift from the one-to-one ratio observed just five years ago. Solar energy investment, in particular, is set to surpass investment in oil production for the first time.

Low-emissions electricity technologies, led by solar, are expected to account for nearly 90 percent of the investment in power generation. Consumers are also investing in electrified end-uses, as evidenced by double-digit annual growth in global heat pump sales since 2021. Electric vehicle sales are projected to increase by a third this year, following a surge in 2022.

Low-emissions electricity technologies, led by solar, are expected to account for nearly 90 percent of the investment in power generation. Consumers are also investing in electrified end-uses, as evidenced by double-digit annual growth in global heat pump sales since 2021. Electric vehicle sales are projected to increase by a third this year, following a surge in 2022.

Several factors have contributed to the boost in clean energy investments in recent years. These include periods of robust economic growth, volatile fossil fuel prices that raised concerns about energy security (especially after Russia’s invasion of Ukraine), and enhanced policy support through initiatives such as the US Inflation Reduction Act and actions in Europe, Japan, China, and other regions.

Spending on upstream oil and gas is expected to rise by 7 percent in 2023, bringing it back to 2019 levels. However, most of the few oil companies investing more than before the Covid-19 pandemic are large national oil companies in the Middle East. Despite some fossil fuel producers enjoying record profits in the previous year due to higher fuel prices, a majority of this cash flow has been allocated to dividends, share buybacks, and debt repayment rather than reinvested in traditional supply.

Nevertheless, the expected rebound in fossil fuel investment suggests that it will exceed the levels required in 2030 to achieve the IEA’s Net Zero Emissions by 2050 Scenario. Global coal demand reached a record high in 2022, and coal investment this year is projected to be nearly six times the levels envisioned for 2030 in the Net Zero Scenario.

In 2022, the oil and gas industry allocated less than 5 percent of its upstream spending to low-emissions alternatives like clean electricity, clean fuels, and carbon capture technologies. This level has seen little change from the previous year, although some larger European companies have a higher share of investment in these areas.

The greatest shortfalls in clean energy investment are observed in emerging and developing economies. While there are some positive developments, such as dynamic investments in solar in India and renewables in Brazil and parts of the Middle East, many countries face obstacles such as higher interest rates, unclear policy frameworks, market designs, weak grid infrastructure, financially strained utilities, and a high cost of capital.