The latest BNEF report has revealed the share of top suppliers in the global wind turbine market for 2023.

The leading suppliers in the wind turbine market in 2023 include: Goldwind (16.4 percent), Envision (15.4 percent), Vestas (13.4 percent), Windey (10.4 percent), Mingyang (9 percent), GE (8.1 percent), Sany (7.9 percent), Siemens Gamesa (7.7 percent), Nordex (6.7 percent), and Dongfang Electric (6 percent), BNEF report said.

In 2022, the BNEF report said Goldwind (12.7 percent), Vestas (12.3 percent), GE (9.3 percent), Envision (8.3 percent), Siemens Gamesa (6.8 percent), Mingyang (6.8 percent), Windey (6.4 percent), Nordex (4.7 percent), Sany (4 percent) and CRRC (3.2 percent) were the top wind turbine suppliers.

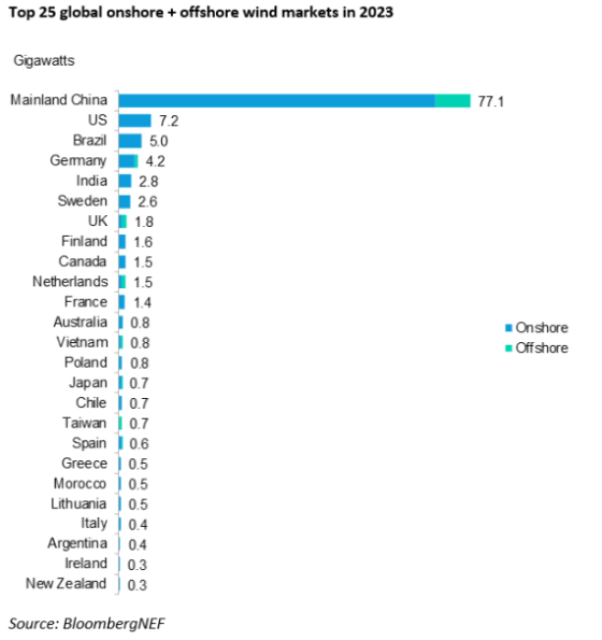

The global wind sector witnessed unprecedented growth, with capacity additions soaring to 118GW in 2023, BloombergNEF (BNEF) said.

The surge, outlined in BNEF’s 2023 Global Wind Turbine Market Shares report, marks a 36 percent increase compared to the previous year, driven chiefly by exponential growth in China, the world’s largest wind market. The report highlights that a substantial portion of the new capacity, totaling 107GW, was installed on land, while 11GW was deployed offshore.

China’s Goldwind has maintained its leading position as the foremost wind turbine supplier globally. Goldwind’s commendable feat of commissioning 16.4GW of projects in 2023, with a significant 95 percent concentrated within China, solidifies its dominance in the industry.

Notably, another Chinese player, Envision, secured the second spot by adding 15.4GW, propelled by the unprecedented wind energy boom in China. Danish firm Vestas clinched the third position with 13.4GW, emerging as the sole European manufacturer among the top five, while Windey and Mingyang claimed the fourth and fifth positions respectively.

Analysts at BNEF underscored the heavy reliance of Chinese turbine manufacturers on their domestic market, with a staggering 98 percent of their capacity additions concentrated within China.

Analysts at BNEF underscored the heavy reliance of Chinese turbine manufacturers on their domestic market, with a staggering 98 percent of their capacity additions concentrated within China.

However, there is a discernible trend of Chinese firms expanding their footprint in foreign markets, with 1.7GW of wind projects commissioned across 20 overseas markets in 2023, nearly triple the number observed in 2018.

This expansion is attributed in part to significant reductions in turbine prices, enabling Chinese companies to compete more aggressively in the global market. Goldwind and Envision emerged as frontrunners in this international expansion, with substantial installations abroad.

The dynamics of the global wind market saw a shift as US-based turbine manufacturer GE slipped to the sixth position in 2023, witnessing a 35 percent decline in installations in its home market. The drop reflects the lowest wind additions in the United States since 2017. Nonetheless, there are optimistic indicators for accelerated growth, such as a surge in US turbine orders following new subsidies introduced under the Inflation Reduction Act.

In the offshore wind industry, Chinese manufacturer Mingyang made significant strides, doubling its annual installations to almost 3GW in 2023 and claiming the top spot globally for the first time. This marks a departure from Siemens Gamesa’s longstanding dominance in offshore wind.

Mainland China retained its status as the primary market for offshore wind, accounting for over two-thirds of global additions, while the UK and the Netherlands maintained their positions as key players in offshore wind development.

Beyond China and the US, regions like the European Union and Brazil showcased remarkable growth in wind energy installations, setting new records and doubling capacities. The collective efforts signal a promising trajectory for global wind energy expansion, offering hope for a greener and more sustainable future.

Baburajan Kizhakedath