The 2024 Global Offshore Wind Report from the GWEC (Global Wind Energy Council) has revealed the key challenges in developing economies.

To meet global climate goals and deploy offshore wind in line with global targets, the following are required:

More capital investment in offshore wind and other renewable energy (RE) in emerging market and developing economy (EMDE) countries.

Addressing insufficient investment due to risk perceptions that may not accurately reflect the actual underlying risks (e.g., risks may be overstated).

Utilising blended finance as a necessary part of the solution to address these risk perceptions.

Continuing to use project finance as the preferred financing method for offshore wind, as it is for many large infrastructure projects.

Assessing the ability of concessional and blended finance in their current forms to scale sufficiently to meet the multi-trillion dollar needs of EMDEs through 2030 and beyond to 2050.

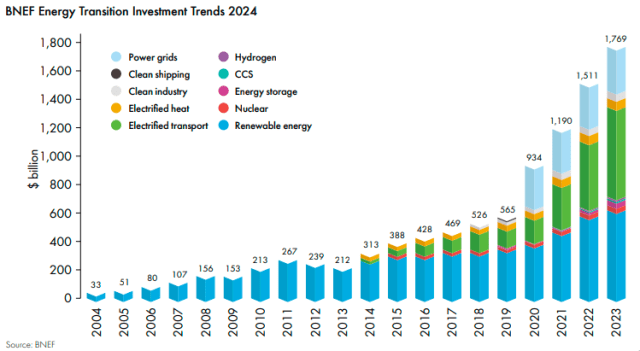

The current situation

Bloomberg New Energy Finance (BNEF) recently released its Energy Transition Investment Trends 2024. This report noted that in 2023, $1.77 trillion was invested in the energy transition, with the biggest largest amounts going to renewable energy (RE) and grids (combine almost $1 trillion combined).

After the electricity sector, electrified transport was the largest destination of energy transition capital, which, of course, needs to run on carbon- free RE to power it to be truly clean. To meet the Paris accord’s 1.5°C target as well as the net-zero commitments of many countries and companies, in addition to COP28’s pledge to triple renewable energy, BNEF states that it would require $12 trillion of investment in the power system up until 2030 – an average of $2 trillion per year starting in 20248 . This represents a significant increase from current annual investments into RE, with much of this investment needing to be directed towards emerging markets and developing economies (EMDEs).

However, recent history demonstrates that investments in RE in EMDEs are falling short. The graphic on below illustrates the total clean energy investment by year by category (EMDE, China and advanced economies).

When comparing investment in clean energy to GDP, EMDE countries receive less investment compared to either China or the advanced economies. It is critical to bring more RE and other clean energy sources to EMDEs.

Over the past decade, more than 95 percent of the increase in greenhouse gas emissions has occurred in EMDEs, and these countries will be the source of 98 percent of world population growth by the end of this decade. EMDE countries clearly need more investments in clean energy.

The industry can achieve that by accelerating the deployment of offshore wind. Offshore wind is a critical building block of any decarbonised future. Indeed, in many of the fast-growing EMDEs in Asia such as Vietnam, the Philippines, and India, offshore wind can provide large-scale, continuous power and is therefore seen as a key energy transition technology.

However, in many of these countries (excluding China), the industry faces relatively high financing costs due to the perceived risks. This poses a challenge because when the cost of capital (weighted average cost of capital or WACC) is 1 percent higher, total CAPEX costs for an offshore wind project increases by approximately 8 percent. Thus, a higher cost of capital plays an outsized role in the overall costs of offshore wind.

The increase in the cost of finance for many offshore wind projects is evident, with key interest rate indices (such as SOFR) rising from 1 percent or 2 percent in 2019 to near 0 percent in 2020 and 2021, to 5.4 percent in May 2024.

On top of the indices, banks typically charge premiums that depend upon their view of in-market, technology and other risks related to the project. While some of the risks can be quantified and mitigated (e.g. through insurance, monitoring requirements, government guarantees, currency hedging, etc.), many cannot and rely on the ‘comfort’ level of the banks.