The latest WindEnergy trend:index (WEtix) survey reveals that confidence in the global wind energy sector has weakened significantly compared with the fourth quarter of 2025, despite continued expectations for market growth. While industry participants remain broadly optimistic about future developments in both onshore and offshore wind energy, the pace of market momentum has slowed across most regions, highlighting growing concerns over policy implementation, permitting challenges, grid infrastructure, and investment conditions.

Europe and Germany Lose Momentum in Wind Energy Expansion

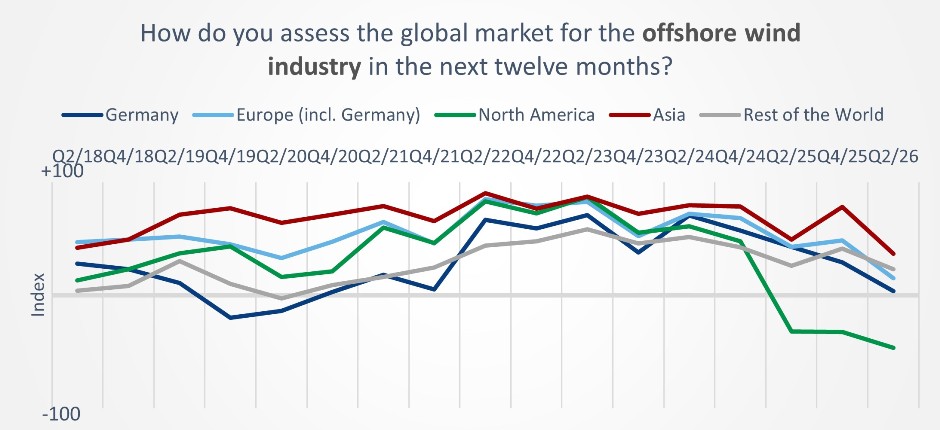

The survey indicates that Germany and Europe are operating at “half-throttle” compared with the stronger sentiment recorded six months earlier. Both onshore and offshore wind segments experienced noticeable declines in market ratings.

Although Europe continues to maintain positive assessments overall, several indicators for Germany and the wider European market are only marginally above the neutral index threshold. Industry stakeholders believe growth opportunities remain, but current market conditions are viewed much more cautiously than at the end of 2025.

The weakening sentiment reflects concerns about project approvals, grid connection delays, financing uncertainties, and supply chain challenges that continue to affect project development across the continent.

Asia Remains the Strongest Wind Energy Market

Asia continues to receive the highest ratings among all regions surveyed, maintaining its position as the leading growth market for both onshore and offshore wind power.

However, even Asia is showing signs of slowing optimism. Compared with the previous survey, industry expectations for the region have weakened noticeably. Despite this decline, Asia remains the most attractive region for future wind energy investments.

The “Rest of the World” category also remains in positive territory, though confidence levels are considerably lower than those recorded at the end of 2025.

North America Emerges as the Weakest Region

North America remains the most challenging market in the global wind energy industry. The survey shows that nearly all evaluated segments scored below the neutral index value, making North America the clear negative outlier.

Respondents cited changing energy and environmental policies as a major obstacle to future wind power development. Regulatory uncertainty and shifting policy priorities are creating challenges for both onshore and offshore wind investments across the region.

The survey findings suggest that policy consistency remains a critical factor in attracting long-term renewable energy investments.

Business Environment Remains the Biggest Barrier

According to the WEtix survey, ambitious political targets alone are insufficient to accelerate wind energy deployment.

Industry participants identified several critical factors that continue to limit market growth:

Faster permitting and approval procedures

Expansion of transmission and grid infrastructure

Greater investment security

Stronger and more resilient supply chains

Respondents consider these areas the most significant barriers preventing the wind sector from reaching its full potential. The survey highlights that successful wind energy markets require supportive business environments in addition to renewable energy targets.

Wind Turbine Size Growth Begins to Stabilize

One of the most notable findings from the survey is the stabilization of turbine size expectations for 2030.

Industry respondents expect newly installed onshore wind turbines to achieve an average rated capacity of approximately 8.3 megawatts (MW) by 2030.

For offshore wind projects, the expected average turbine size has settled at approximately 19.1 MW, slightly lower than forecasts reported in recent surveys.

This trend suggests that the industry is shifting away from the rapid escalation of turbine dimensions seen in previous years. Manufacturers and developers are increasingly prioritizing technologies that are economically viable, technically reliable, and commercially proven.

Regional Supply Chains Gain Strategic Importance

The survey also examined expectations regarding domestic and continental value chains.

Results show that Europe and Asia are expected to maintain significantly stronger domestic supply chains compared with North America and other regions. Germany stands out for achieving an almost perfect balance between domestic and international value creation.

These findings underline the growing strategic importance of localized manufacturing, regional sourcing, and domestic industrial ecosystems in enhancing the competitiveness of wind energy markets.

As governments increasingly prioritize energy security and economic development, regional supply chains are expected to play a larger role in future wind power investments.

Global Industry Participation Ensures Broad Market Representation

The latest WEtix survey attracted substantial participation from across the wind energy sector. A total of 718 respondents contributed to the survey between mid-March and early May 2026, while 399 respondents completed all or nearly all sections of the questionnaire.

Participants represented all major stages of the global wind energy value chain, providing a comprehensive view of both onshore and offshore market conditions worldwide.

Outlook for the Global Wind Industry

The 2026 WindEnergy trend:index survey highlights a global wind industry that remains fundamentally optimistic about long-term growth but is becoming increasingly cautious about near-term market conditions. Asia continues to lead the sector, Europe faces slowing momentum, and North America remains constrained by policy uncertainty.

With turbine sizes stabilizing at 8.3 MW onshore and 19.1 MW offshore, and with 718 industry professionals contributing insights, the survey emphasizes that future wind energy growth will depend less on ambitious targets and more on practical measures such as streamlined permitting, stronger grids, investment certainty, and resilient regional supply chains.

BABURAJAN KIZHAKEDATH