A new report released by the Global Wind Energy Council (GWEC) at COP30 highlights how blended finance and innovative financial instruments can accelerate offshore wind development in emerging Asia-Pacific markets such as the Philippines and Vietnam. The report outlines barriers, financing gaps, and the pathways needed to reduce project costs, build investor confidence, and scale deployment across the region.

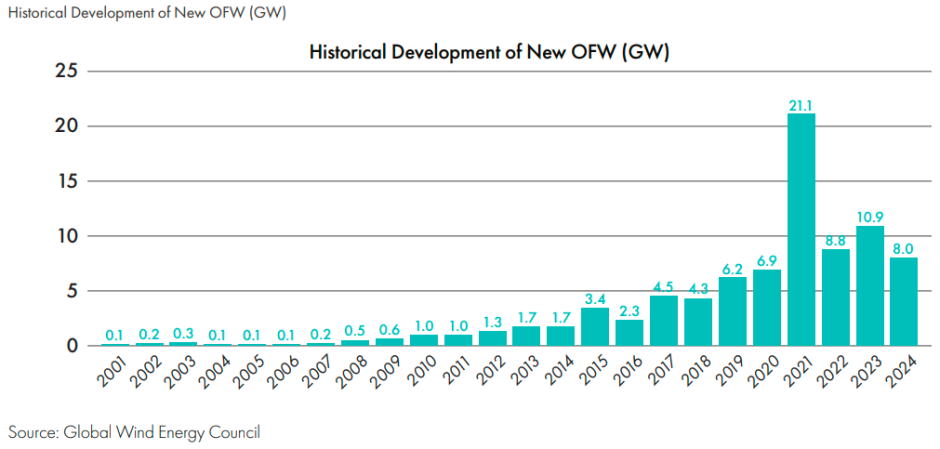

Global offshore wind capacity has expanded rapidly over the past two decades, rising from 2.5 GW in 2010 to 83 GW by the end of 2024. The sector recorded its strongest year in 2021 with 21.1 GW of new installations, although growth has since softened due to rising commodity prices, higher labour and logistics costs, and increased cost of capital caused by interest rate hikes and higher risk premiums. These pressures have slowed project timelines and resulted in undersubscribed auctions. Annual additions reached 8.8 GW in 2022, climbed to 10.9 GW in 2023, and adjusted to 8 GW in 2024. However, a more robust project pipeline indicates stronger growth expected in 2025.

Long-term projections highlight the scale of opportunity. IRENA estimates that the world will need around 2 TW of offshore wind capacity by 2050 to meet global climate goals and stay well below 1.5 degrees Celsius of warming. Meanwhile, World Bank analysis across 75 emerging markets points to more than 16.2 TW of offshore wind resource potential, including 5.5 TW from fixed-bottom installations and 10.7 TW from floating wind.

The Asia-Pacific region continues to dominate global offshore wind. By the end of 2024, APAC and Europe together accounted for 98.9 percent of global offshore wind capacity, with APAC leading at 46.3 GW in operation compared to Europe’s 36 GW. China remained the world’s largest offshore wind market in 2024, adding 4.0 GW and raising its total capacity to 41.8 GW. Other Asian markets also expanded, with Taiwan commissioning 933 MW, Japan 112 MW, and South Korea 100 MW during the year.

1. Blended Finance Is Critical for Offshore Wind Expansion in Emerging Markets

The GWEC report emphasizes that offshore wind development in emerging Asia-Pacific requires blended finance — mixing commercial capital with concessional loans, guarantees, and first-loss capital. Unlike mature markets, early-stage risk levels in the Philippines and Vietnam demand stronger support from DFIs and MDBs.

2. Bankable Projects Depend on Macro-Level and Deal-Level Features

A project becomes bankable when physical infrastructure is ready, supply chains exist, policies are clear, and pricing mechanisms are transparent. At the deal level, strong PPAs, competitive tariffs, clear risk allocation, developer experience, and creditworthy offtakers are essential.

3. DFIs and MDBs Currently Play a Limited Role in Offshore Wind

While offshore wind in advanced markets has progressed with minimal DFI/MDB involvement, emerging economies cannot rely on commercial lenders alone. Current engagement is sparse, and the report highlights the need for tailored, country-specific financing solutions.

4. Key Barriers Include Regulatory Uncertainty and Infrastructure Gaps

Macro challenges such as unclear regulatory frameworks, limited port capacity, grid constraints, and weak supply chains hinder timely project execution. Deal-level barriers include currency risks, high capital needs, lack of bankable PPAs, and hesitation from first-mover developers.

5. Blended Capital Stacks Can Dramatically Reduce Offshore Wind Costs

Modeling of a 500 MW offshore wind project shows that a fully blended structure—mixing commercial debt, concessional loans, export credit guarantees, and grants—cuts financing costs sharply. Weighted average cost of capital drops from 11.72 percent to 6.54 percent in the Philippines and from 12.23 percent to 6.82 percent in Vietnam, significantly reducing final tariffs.

6. Tariffs Can Drop Up to 40 Percent Through Optimized Financing

Using blended finance, offshore wind tariffs fall from 16.20 PHP/kWh to 10.50 PHP/kWh in the Philippines and from 4,579.60 VND/kWh to 2,931.45 VND/kWh in Vietnam. This improves affordability, strengthens DSCR, and builds lender confidence.

7. Governments Should Establish Clear Offtake and Pricing Frameworks

The report urges governments to define transparent offtake structures, adopt viable long-term PPAs, explore Contracts for Difference, and frequently update frameworks. Clear revenue pathways are pivotal for attracting private and institutional capital.

8. Developers Must Collaborate on Policy and Innovate Structuring Models

Developers are encouraged to work closely with policymakers on tariff design, risk sharing, and auction structures. Creating consortiums can help pool expertise, share risks, and improve project competitiveness in emerging markets.

9. DFIs/MDBs Should Increase Concessional Debt and Technical Support

DFIs and MDBs can unlock early-stage offshore wind investments by offering below-market loans, supporting port and grid upgrades, and expanding capacity-building programs. Their due diligence also adds a “halo effect,” pulling in commercial lenders.

10. Climate Funds and ECAs Hold Key Roles in Risk Reduction

Climate funds can provide first-loss capital, grants, and concessional financing to de-risk projects. Export credit agencies should supply credit guarantees and insurance, backing large-scale investments and enabling longer-tenor, lower-cost debt while supporting cross-border supply chain partnerships.

Baburajan Kizhakedath