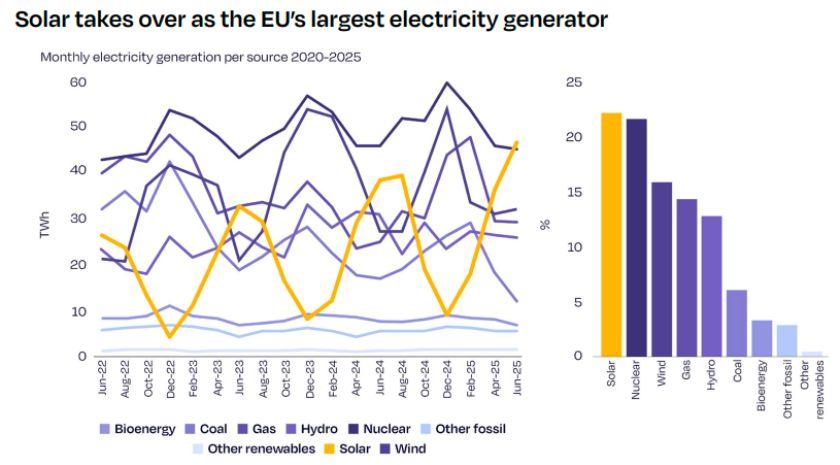

Despite solar energy becoming the largest source of electricity in the European Union in June 2025 — accounting for 22.1 percent of the power mix — and the bloc being on the verge of meeting its 2025 RePowerEU target of 400 GWDC of solar capacity, Europe is now facing its first significant solar market downturn in nearly a decade. As it stands, the EU is expected to fall short of its more ambitious 2030 target of 750 GWDC, with current trends pointing toward only 723 GWDC being installed by the end of the decade, SolarPower Europe said in a report.

The main reason behind this shortfall is a sharp slowdown in solar deployment growth. After two years of exceptional expansion in 2022 and 2023 — growing by 47 percent and 51 percent respectively — growth flattened to just 3.3 percent in 2024. In 2025, the market is projected to contract by 1.4 percent, marking the first decline in nearly ten years.

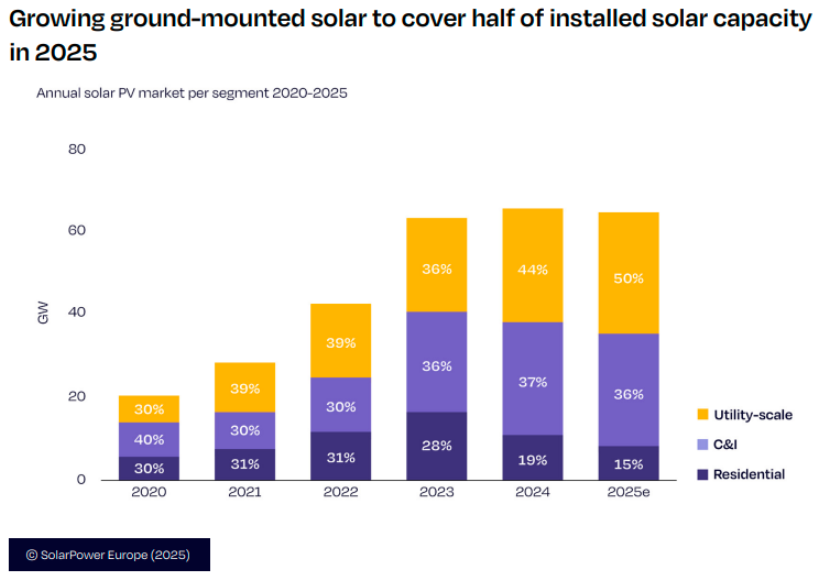

This downturn is largely driven by the rooftop solar segment, particularly residential systems. Falling electricity prices and the withdrawal or weakening of government incentives have led households and small businesses in several key Member States to delay or cancel installations. As a result, residential solar’s contribution to new capacity is expected to drop from 30 percent (2020–2023) to just 15 percent in 2025.

Several rooftop solar installation projects across Europe have faced cancellations or delays due to a range of issues including financial constraints, policy uncertainty, and grid limitations. In Germany, some homeowners have withdrawn applications for rooftop solar systems after subsidy cuts and delays in processing grid connection requests.

The size of the 2025 rooftop market is expected to show an 11 percent decline to 32.4 GW, down from 36.3 GW in 2024, which would constitute about half of the total added solar capacity in 2025, according to Michael Schmela and Jonathan Gorremans at SolarPower Europe.

In the Netherlands, the proposed phase-out of net metering has led to a drop in new installations and the cancellation of planned rooftop projects by households concerned about return on investment. In Spain, local permitting delays and high interest rates have discouraged small-scale residential solar investments, leading to a decline in confirmed rooftop installations.

Similarly, in Italy, a slowdown in incentive payments and regulatory changes have caused some consumers to abandon solar plans midway. In France, concerns over rooftop system payback periods and a lack of skilled installers have resulted in project backlogs and contract terminations.

While utility-scale solar remains more resilient—bolstered by favorable financing mechanisms and corporate Power Purchase Agreements (cPPAs)—it is not immune to headwinds. The recent drop in electricity prices has made PPA buyers more hesitant, causing a 41 percent decline in newly signed solar PPAs in Q2 2025 compared to Q1. Although auctions and tenders continue to attract competitive pricing, the uncertainty in long-term contract support poses risks to sustained growth.

To close the gap toward the 2030 target, the EU must urgently enhance the value of solar electricity in the grid. This includes ramping up investments in energy system flexibility, particularly battery storage, which is essential for integrating variable solar output and improving project economics. While long-term grid investments are necessary, short-term acceleration in storage deployment is critical to keeping solar momentum alive.

Baburajan Kizhakedath