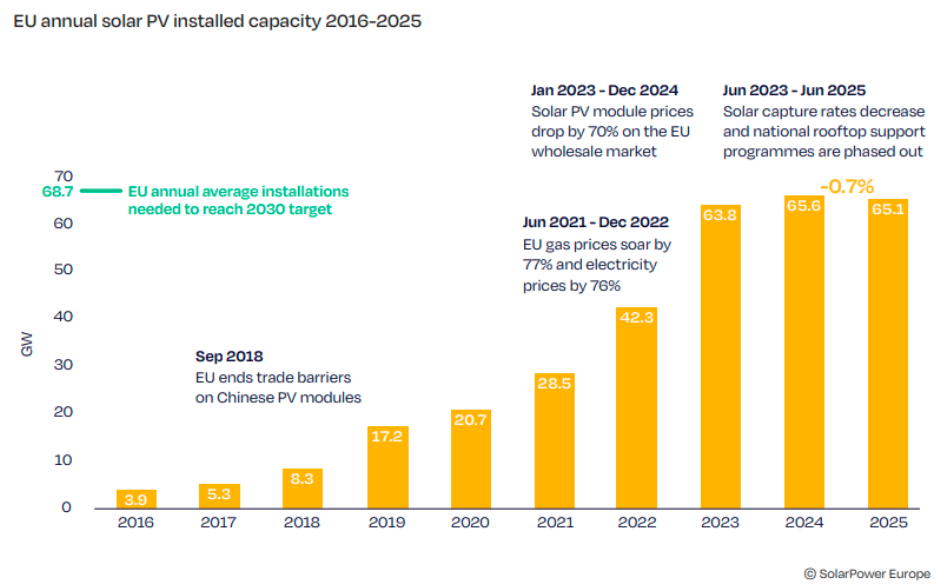

The European Union solar market is entering a phase of cooling after years of rapid expansion, according to Solar Power Europe. The EU is expected to install 65.1 GW of new solar PV capacity in 2025, a slight 0.7 percent decline from the 65.6 GW added in 2024. This slowdown follows a noticeable deceleration last year when annual growth slipped to 2.8 percent.

The easing of the energy crisis has softened the urgency for households and businesses to invest in rooftop solar. While gas and electricity prices remain high, support schemes in major markets have been phased out, reducing incentives for residential and commercial installations. For utility-scale developers, auctions and corporate PPAs still provide momentum, but challenges such as grid congestion, rising negative price events and policy uncertainty are affecting project bankability.

Compared to last year’s projection of a 70 GW market for 2025, the new estimate is 7 percent lower, driven mainly by sharper-than-expected declines in rooftop demand. This trend highlights how sensitive households and businesses are to policy changes and market conditions. It also signals a warning for EU policymakers who aim to maintain the region’s solar momentum toward 2030.

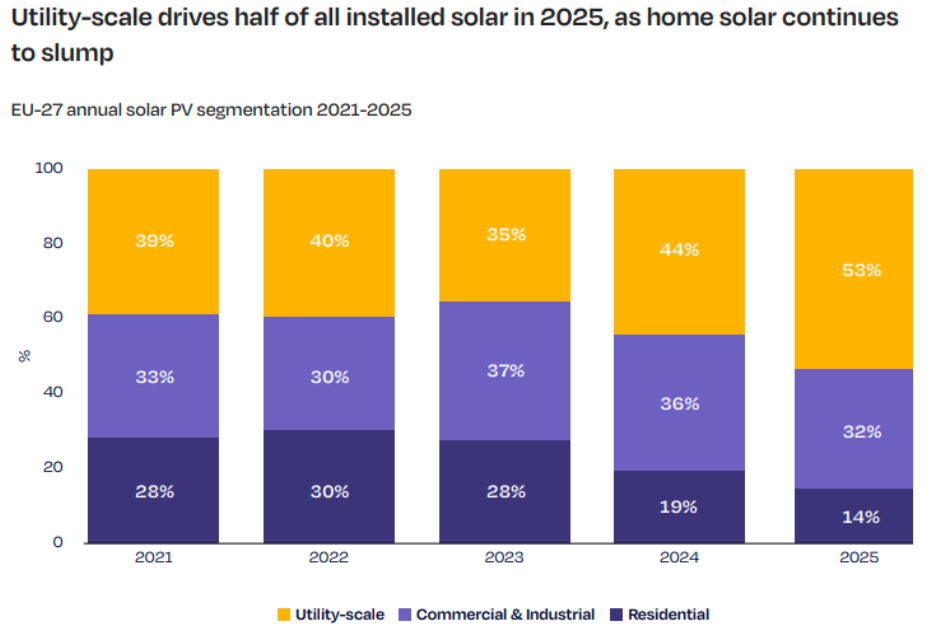

A key shift emerges in 2025: utility-scale installations become the primary engine of growth, accounting for more than half of annual additions for the first time. On a cumulative basis, rooftop systems still dominate with a 61 percent share, but utility-scale capacity continues to expand its footprint.

Solar’s contribution to the EU power mix continues to rise sharply. The technology is expected to deliver 13.4 percent of the region’s electricity in 2025, up from 11.6 percent in 2024 and 9.7 percent in 2023. The rapid deployment of solar and wind is increasingly displacing fossil fuels.

Between 2021 and 2024, the gas share fell from 19.0 percent to 15.3 percent, while coal dropped from 14.7 percent to 9.9 percent. In June 2025, solar became the EU’s largest single power source for the first time, providing 22 percent of total electricity generation. Combined, solar and wind are set to supply over 30 percent of EU electricity in 2025, surpassing all fossil fuels combined.

Seasonal output patterns are also shifting. Spring shows the strongest growth, with March to May production two to three times higher than five years earlier. Summer continues to set new output records, while autumn generation has nearly doubled since 2020. Winter solar is also improving, with January generation covering more than 4.5 percent of EU electricity demand.

By September 2025, solar had already generated more electricity than during the whole of 2024, reaching 312 TWh in nine months.

Market dynamics are changing significantly across segments. Residential solar sees the sharpest decline in 2025, with 19 markets contracting and reducing the segment’s share of annual installations to 14 percent, half of what it was in 2023. The phase-out of support schemes and slow expansion beyond early adopters contribute to this drop. However, plug-in or balcony solar systems are growing in popularity, thanks to low upfront costs and simple setup.

Commercial and industrial installations are more stable but still soften, with the segment’s share falling from 37 percent in 2023 to about 32 percent in 2025. Growth is becoming increasingly concentrated in a smaller number of countries.

Utility-scale solar remains the most resilient, supported by auctions and PPAs from previous years that are now reaching completion. On a cumulative basis, utility-scale systems are expected to account for 39 percent of installed capacity by the end of 2025.

Looking ahead, EU solar installations are projected to decline again in 2026 and 2027 before moving into a slow recovery toward 2030. In the Medium Scenario, installations follow a U-shaped trajectory, with two years of single-digit contraction followed by a gradual rebound to reach 67 GW in 2030. The Low Scenario places installations near 50 GW, while the High Scenario anticipates continued annual growth throughout the decade.

Several factors shape this downturn. Utility-scale projects face rising profitability challenges, pushing developers toward hybrid solar and storage models. Rooftop demand is expected to remain subdued through 2026 and 2027 due to scheme phase-outs, slow policy support for self-consumption and lower retail electricity prices. A stabilisation is expected from 2027 onward as electrification accelerates, energy-sharing frameworks expand and new rooftop requirements come into effect.

The cumulative trajectory suggests that current conditions are insufficient for the EU to meet its 750 GW solar target by 2030. The Medium Scenario reaches 718 GW, leaving a shortfall of more than 30 GW. Only the High Scenario, which reaches 810 GW, aligns with the EU’s 2030 ambition.

Both rooftop and utility-scale markets will continue to expand cumulatively, though at different speeds. Rooftop capacity is projected to grow from 247 GW in 2025 to 397 GW by 2030. Utility-scale solar grows faster, doubling from 159 GW to 321 GW. As large project pipelines mature and permitting improves, utility-scale installations will continue gaining ground, even though rooftop systems retain the majority share.

Baburajan Kizhakedath