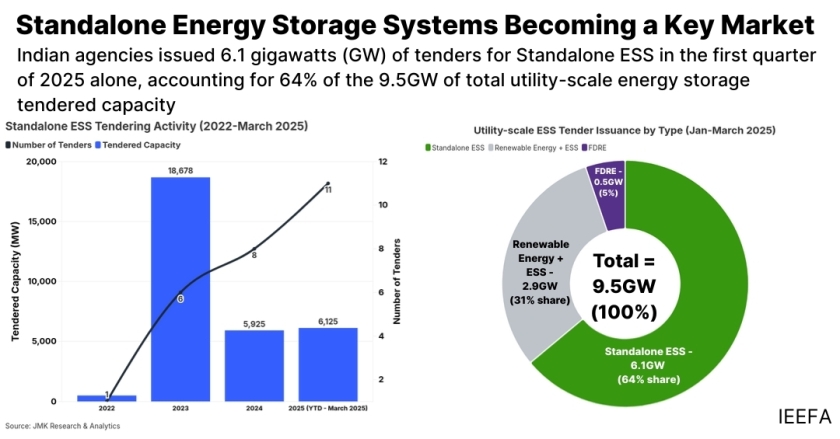

Standalone Energy Storage Systems (ESS) are rapidly emerging as a cornerstone of India’s utility-scale energy storage landscape, with recent data showing that they accounted for 64 percent of total ESS tenders issued between January and March 2025.

According to a new report by the Institute for Energy Economics and Financial Analysis (IEEFA) and JMK Research & Analytics, various government agencies tendered a remarkable 6.1 gigawatts (GW) of standalone ESS capacity during the first three months of the year.

The report emphasizes that standalone ESS are particularly well-suited to accelerate the deployment of variable renewable energy (VRE) resources across India, an essential step in achieving a resilient and flexible grid.

Energy Specialist Charith Konda, a contributing author of the report, highlights how standalone ESS function as flexible, independent assets that respond directly to grid demands rather than being tethered to generation constraints, thereby offering enhanced network stability and more efficient energy utilization.

One of the major factors fueling this momentum is the government’s Viability Gap Funding (VGF) scheme, which provides up to 30 percent capital expenditure support for standalone battery energy storage system (BESS) projects. This financial support has played a critical role in mitigating the high initial capital costs typically associated with BESS deployments, thus making projects far more viable economically. Prabhakar Sharma, Senior Consultant at JMK Research & Analytics and co-author of the report, notes that recent auctions in Maharashtra and Rajasthan achieved tariffs as low as Rs 219,000 to Rs 221,000 per megawatt per month (approximately US$2,561 to $2,586/MW/month), a nearly 40 percent drop compared to similar non-VGF supported projects.

Ownership and operation models for standalone ESS are becoming increasingly diverse. Utilities, grid operators, and third-party companies can own these systems, and newer business models like Energy Storage as a Service (ESaaS) are emerging. ESaaS arrangements lower the entry barriers by offering storage services through subscription or pay-per-use models, providing a flexible alternative for users who might otherwise be deterred by the high upfront costs. The success and attractiveness of standalone ESS are drawing in not just traditional large-scale power producers like JSW Energy, Greenko, and Torrent Power, but also newer and smaller players such as Pace Digitek, Oriana Power, Kintech Synergy, and Bondada Engineering, signaling the broadening base of competition and innovation in the sector.

Despite the promising growth trajectory, the standalone ESS market in India faces several significant challenges. One immediate concern is the delay or cancellation of power sale and storage agreements, often driven by buyers holding out for anticipated reductions in battery costs. According to Pulkit Moudgil, Research Associate at JMK Research & Analytics, this uncertainty has already resulted in the cancellation of around 6.4GW of previously awarded storage capacity. Moreover, the market is grappling with structural barriers, including a limited number of utility-scale equipment vendors, the lack of a robust domestic battery manufacturing ecosystem, and heavy reliance on imports of critical minerals like lithium and cobalt. These dependencies expose the sector to global supply chain disruptions and geopolitical risks. In addition, smaller developers are facing difficulties in accessing affordable financing, largely because investors remain cautious due to the early-stage nature of the market and the long timeframes needed to recover their investments.

Looking ahead, the standalone ESS market in India stands at a crucial inflection point. While the initial surge in tenders and deployments paints a promising picture, sustained policy support, streamlined regulatory frameworks, and strategic investments in domestic manufacturing capabilities and resilient supply chains will be vital for overcoming current barriers. If these challenges are addressed effectively, India’s standalone ESS sector has the potential to not only reinforce the country’s renewable energy ambitions but also to establish itself as a key pillar in the global energy storage industry.

Baburajan Kizhakedath