The U.S. Energy Information Administration has released the Annual Energy Outlook 2026 (AEO2026), offering a comprehensive view of how the United States energy system could evolve through 2050 under multiple scenarios shaped by technology, policy, and market dynamics.

Described as a framework for exploring alternative futures rather than a predictive report, AEO2026 highlights the growing influence of artificial intelligence, data centers, and clean energy in transforming energy demand and supply patterns.

Energy Efficiency Keeps Overall Consumption Stable

Despite steady economic growth projected between 1.2 percent and 2.2 percent annually, total U.S. energy consumption is expected to remain relatively flat or decline slightly through 2050 in most scenarios. This trend is driven by continued advancements in energy-efficient technologies across industries.

Energy demand in the transportation sector is projected to decline, while residential and commercial consumption remains stable, even as electricity demand rises due to digital infrastructure expansion.

Data Centers and AI Drive Electricity Demand Growth

A key finding of AEO2026 is the rapid rise of data center energy consumption, fueled by the expansion of AI workloads. After more than a decade of stagnant electricity demand, U.S. consumption has grown 2.1 percent annually over the past five years.

Electricity demand is projected to grow at 0.9 percent to 1.6 percent annually through 2050. Data center server energy use could reach 818 billion kilowatthours by 2050 in high-demand scenarios, more than 16 times 2020 levels.

Commercial buildings, which house most data center operations, are expected to account for the largest share of electricity growth, particularly in regions such as Virginia and Texas.

Power Capacity Expansion Accelerates

To meet rising electricity needs, total installed generation capacity is projected to increase between 50 percent and 90 percent by 2050. The energy mix will be dominated by natural gas, solar, and wind, which together could account for around 80 percent of total electricity generation.

While natural gas generation increases in absolute terms, its share remains relatively stable, highlighting its ongoing role in grid reliability and price setting.

Natural Gas Production and Infrastructure Growth

U.S. natural gas production is forecast to grow significantly, rising from 107 billion cubic feet per day in 2025 to between 133 and 151 Bcf/d by 2050. Growth is expected to be strongest in the Appalachian Basin, supported by both domestic consumption and export demand.

This expansion will require major investments in pipeline infrastructure to transport gas efficiently to key demand centers, including the Gulf Coast.

Oil Output Stabilizes, Exports Continue

U.S. crude oil production is projected to remain relatively stable, declining slightly from 13.6 million barrels per day in 2025 to between 12.4 million and 12.7 million barrels per day by 2050. The Permian Basin will remain the primary driver of onshore oil production.

The United States is expected to continue as a net exporter of petroleum, with growing exports of refined products and liquids.

Coal Declines Amid Policy Uncertainty

Coal demand continues its long-term decline, largely driven by plant retirements and environmental regulations. If current emissions rules remain in place, coal-fired power generation could nearly disappear by 2050.

In scenarios without such regulations, coal retains a small share of the energy mix, though still significantly reduced compared to current levels.

Electricity Demand Patterns Impact System Costs

The report also highlights how the timing of electricity demand affects grid costs. While electric vehicles and data centers contribute significantly to demand growth, they account for only 10 percent to 25 percent of total electricity consumption by 2050.

However, their usage patterns influence peak demand and system load factors, affecting infrastructure investments and electricity pricing.

Renewables and Gas Lead Future Energy Mix

Across all scenarios, solar, wind, and natural gas remain central to the U.S. energy transition. Their combined share of electricity generation is expected to rise from about 60 percent in 2025 to nearly 80 percent by 2050.

Meanwhile, nuclear energy remains stable in output but declines in overall share, reflecting faster growth in other generation sources.

Strategic Outlook for Energy Transition

AEO2026 underscores the critical role of emerging technologies, particularly AI-driven data centers, in shaping future energy demand. At the same time, the continued expansion of renewables and natural gas highlights a dual-track transition balancing sustainability with reliability.

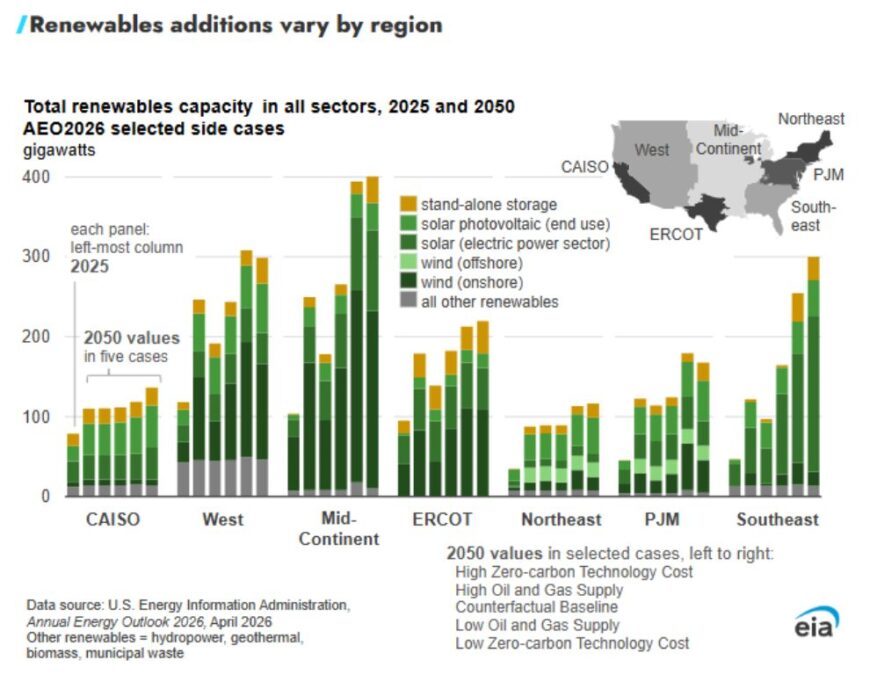

Renewable Capacity Growth Across All Regions

Renewable power capacity is set to expand significantly across every region of the United States through 2050, although the energy mix will vary depending on local resource availability. Wind and solar remain the primary drivers of this expansion, supported by favorable economics and regional resource strengths.

In the Mid-Continent region, renewable capacity is projected to increase between 75 GW and 300 GW, with wind energy contributing the largest share of growth due to abundant low-cost resources and relatively higher natural gas prices.

Solar and Battery Storage Integration Accelerates

Solar capacity is expected to grow between 100 percent and 235 percent by 2050 in most scenarios. The Southeast region leads this expansion, with solar deployment rising twofold in lower-cost scenarios and up to sevenfold when natural gas prices are higher or renewable costs decline.

Energy storage, particularly battery systems, is increasingly being deployed alongside solar projects. These systems help manage solar’s variability by storing excess generation and releasing it during peak demand periods. By 2050, between 2.5 GW and 25 GW of battery capacity is expected to be co-located with solar installations, accounting for up to 10 percent of total storage capacity.

Wind Power Gains Momentum in Key Regions

Wind energy continues to play a central role in the U.S. clean energy transition. In the Mid-Continent region alone, wind capacity could grow by as much as 170 GW compared to 2025 levels. The region’s strong wind resources and cost advantages make it a key hub for future wind development.

Coal Demand Hinges on Policy Direction

Coal consumption in the United States is projected to decline sharply, with future demand largely dependent on environmental policy decisions. If 2024 emissions regulations are fully implemented, coal-fired power generation could nearly disappear by 2050, dropping from 388 million short tons in 2025 to negligible levels.

In scenarios without these regulations, coal remains in the energy mix but still declines significantly, falling to around 150 million short tons by 2050.

Industrial and Steel Sector Shifts Reduce Coal Use

Coal use in the industrial sector is expected to decrease by around 30 percent by 2050, as natural gas and electricity replace coal due to higher efficiency and lower operating costs.

In the steel industry, metallurgical coal demand is also declining as electric arc furnaces gain adoption, reducing reliance on traditional blast furnace methods. This shift lowers coke production and further weakens coal demand.

Coal Exports Provide Partial Offset

Despite declining domestic consumption, U.S. coal exports are projected to increase by approximately 20 percent, rising from 96 million short tons in 2025 to 115 million short tons by 2050. This growth is driven by continued global demand, assuming no major restrictions on international coal trade.

Energy Transition Gains Momentum

The outlook underscores a clear transition toward a cleaner and more diversified energy system in the United States. Renewable energy, supported by battery storage, is set to dominate capacity additions, while coal continues its structural decline.

BABURAJAN KIZHAKEDATH