S&P Global Commodity Insights has released its report detailing the most significant trends in clean energy technology for 2024.

The report outlines key developments that are set to shape the global landscape, including investment projections, cost reductions, offshore wind milestones, and increased focus on decarbonization.

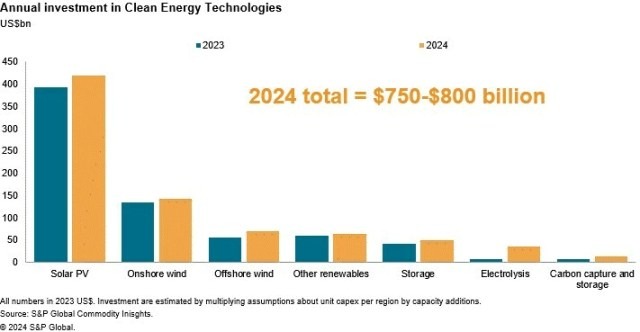

- Clean Energy Technology Investment to Reach Nearly US$800 Billion in 2024 and $1 Trillion by 2030

There will be a substantial increase in clean energy technology (CET) investments, nearing $800 billion in 2024, with solar dominating the investment landscape. This represents a 10 percent to 20 percent surge from 2023 spending levels. The report emphasizes the pivotal role of solar, onshore wind, battery energy storage, and electrolysis in driving this surge.

- Average Capex of Clean Energy Technologies to Decline by 15 percent-20 percent by 2030

Despite challenges in offshore wind and hydrogen sectors, the report highlights an anticipated 15 percent-20 percent decline in the average capital expenditure for clean energy technologies by 2030. This decline is attributed to oversupply and falling raw material prices, especially in solar and battery technologies, which are expected to drop below 2020 levels in 2024.

- Decarbonization at the Core of Clean Energy Technology Manufacturers’ Strategies

A significant shift is observed in clean energy technology manufacturers’ strategies, with a newfound focus on decarbonization. Manufacturers are not only aligning their products with low-carbon electricity resources but also committing to decarbonize operations before 2030. This reflects a broader movement toward increasing transparency and traceability in renewable supply chains.

- Solar and Storage Manufacturers Engage in Price War Due to Oversupply

The report highlights a price war among solar and battery manufacturers as oversupply and falling raw material prices lead to declining prices in modules and batteries. The downstream players, including distributors and installers, face challenges with high inventories, potentially resulting in market consolidation in 2024.

- Record High Offshore Wind Capacity Auctions Expected in 2024

Despite rising capital costs, offshore wind is poised for a milestone year with over 60 GW of new capacity set to be auctioned in at least 17 different markets. This unprecedented surge in auctioned capacity underscores the global commitment to advancing offshore wind technology.

- Western Wind Turbine Giants Face Growing Competition from the East

The global wind turbine supply market is witnessing a shift, with Chinese manufacturers increasingly competing against Western counterparts through lower prices, technological innovation, and new supply chain investments. Western turbine makers face challenges in regaining profitability while safeguarding market share.

- Growing Global Interest in Low-Carbon Hydrogen as Feedstock

The report identifies a surge in global interest in low-carbon hydrogen, driven by subsidies and mandates. Denmark’s green hydrogen production and Middle Eastern facilities contribute to this momentum, indicating a broader trend toward low-carbon hydrogen as a feedstock.

- 2024 a Milestone Year for Technology-Based Carbon Dioxide Removal (CDR)

Advancements in carbon crediting methodologies and significant funding for technology-based carbon dioxide removal (CDR) are driving an unprecedented project pipeline. Buyers are willing to pay a premium for durable and traceable technology-based CDR methods, with the EU expected to adopt a carbon removal certification framework in 2024.

- Efforts to Alleviate Grid Congestion and Permitting Constraints

With a commitment to triple global renewables capacity by 2030, efforts to alleviate grid congestion and permitting constraints are crucial. Increased investment in transmission and distribution, coupled with the facilitation of other renewable technologies, aims to streamline renewable power development globally.

- Transmission System Operators (TSOs) to Assess Flexibility Needs from 2025

As more than 1 TW of wind and solar installations are expected globally in the next two years, TSOs will play a pivotal role in assessing flexibility needs. The report highlights the urgency for increased flexibility assets such as storage and demand response, driven by the growth of intermittent renewable generation. Countries in Europe are mandated to evaluate flexibility requirements biannually, beginning January 2025, ensuring a balanced electricity supply and demand.