India’s clean energy transition is increasingly dependent on rapid deployment of energy storage systems as the country moves toward its ambitious target of 500 GW of renewable energy capacity by 2030. A new report from Institute for Energy Economics and Financial Analysis and JMK Research and Analytics reveals that India’s energy storage sector is witnessing strong growth momentum, but aggressive tariff bidding, financing challenges, and supply chain risks could threaten project viability and execution.

According to the report, India’s cumulative tendered energy storage capacity increased sharply from 6.8 GW in 2018 to 90.7 GW in 2025. Standalone energy storage system (ESS) tenders have emerged as the dominant procurement model, accounting for more than 71 percent of the total energy storage capacity tendered in 2025. Within this category, standalone battery energy storage system (BESS) projects represented 60 percent of total tendered capacity.

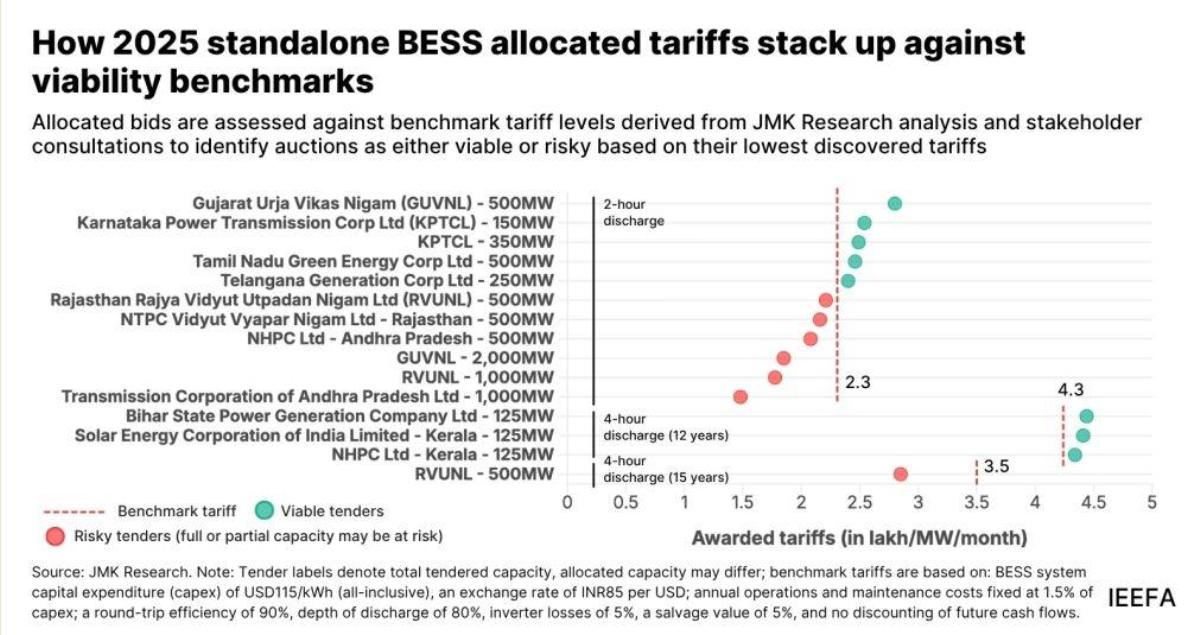

The report highlights that India allocated 10.4 GW of standalone BESS capacity during 2025. The majority of these projects used the 2-hour, 2-cycle configuration, enabling utilities and power distribution companies to manage both morning and evening peak electricity demand within a single day.

Researchers noted that declining battery prices and supportive government initiatives, including viability gap funding for standalone BESS projects, have accelerated the shift toward standalone storage procurement. However, despite this momentum, the report warns that the economic viability of many projects remains uncertain.

Tariffs for standalone BESS projects declined significantly during 2025. The lowest discovered tariff fell to INR1.48 lakh per megawatt per month ($1,576/MW/month) for 2-hour systems, compared to the benchmark tariff estimate of INR2.3 lakh/MW/month ($2,448.95/MW/month). The report estimates that nearly 75 percent of allocated 2-hour BESS capacity now falls into an “at-risk” viability category because discovered tariffs are below realistic project cost levels.

The study found that economically viable projects were mainly concentrated in smaller, early-stage state auctions conducted in Karnataka, Tamil Nadu, Telangana, and Gujarat. Analysts believe that future procurement frameworks will require major reforms to improve long-term project sustainability.

Recommended reforms include introducing cost-reflective tariff floors, implementing stricter bidder eligibility criteria, and strengthening payment security mechanisms. The report also stresses the need to align auction structures with realistic execution timelines and financing conditions.

Execution risks are another major concern for India’s growing BESS market. Financing conditions remain difficult as developers face pressure from declining tariffs, rising battery input costs, and dependence on imported battery supply chains. The report warns that delays of up to 18 months may continue due to financial closure challenges, procurement bottlenecks, and commissioning issues.

Researchers cautioned that lower tariffs could also force developers to compromise on asset quality, potentially affecting long-term operational performance and reliability of storage infrastructure.

Despite near-term risks, the report indicates that energy storage deployment in India will continue to expand rapidly. Around 1.8 gigawatt-hours (GWh) of grid-scale BESS capacity had been installed in India as of March 2026, with most of this capacity added during the final six months of FY2026.

The report also highlights India’s heavy reliance on lithium-ion battery technology and supply chains linked to China. This dependence exposes India’s energy storage ambitions to global supply chain disruptions and raw material volatility.

To reduce these risks, tendering agencies and policymakers are expected to increasingly support alternative storage technologies such as flow batteries and sodium-ion batteries. Analysts believe India’s future energy storage ecosystem will consist of a diversified technology mix, with different battery technologies serving specific use cases, duration requirements, safety standards, and cost structures.

The report concludes that long-term success in India’s energy storage market will depend on domestic manufacturing expansion, strategic critical mineral partnerships, diversified battery technologies, and procurement reforms that balance affordability with sustainable project economics.

BABURAJAN KIZHAKEDATH