The Institute for Energy Economics and Financial Analysis (IEEFA) has released its latest Data Dive report, an analytical tool that tracks natural gas and liquefied natural gas (LNG) demand across 14 major Asian economies. The tool help users compare sectoral gas consumption, domestic production trends, LNG imports, spending patterns, and pricing movements.

The report aims to clarify the drivers of natural gas demand in Asia and assess the risks that could influence future LNG growth. While it does not offer long term forecasts, it provides detailed insights that help explain near term challenges for gas dependent sectors.

Key findings from IEEFA Data Dive

Industrial sector leads regional gas growth

Natural gas usage in the power sector remains the highest in Asia, but the industrial sector has been the largest contributor to demand growth since 2015. Industries such as manufacturing, refining, cement, metals, and chemicals have expanded gas consumption rapidly, led primarily by China, India, South Korea, Indonesia, Malaysia, Vietnam, and Bangladesh.

Power sector demand falls in several major markets

Gas demand in the power sector has fallen since 2015 in Japan, India, Indonesia, Malaysia, Vietnam, and the Philippines. These declines have been driven by nuclear restarts, renewable energy deployment, high gas prices, supply constraints, and government decisions to prioritize gas allocation to non power sectors. The drop in Japan alone contributed to 70 percent of total regional demand decline among the affected countries.

Domestic gas production declines across Asia

Most Asian markets are experiencing falling domestic gas production due to maturing fields, limited discoveries, and higher extraction costs. Exceptions include China and Malaysia. In India, production peaked in 2010 and has struggled to recover. Declining reserves in the Philippines, Thailand, and Bangladesh point to less than ten years of supply left at current production rates.

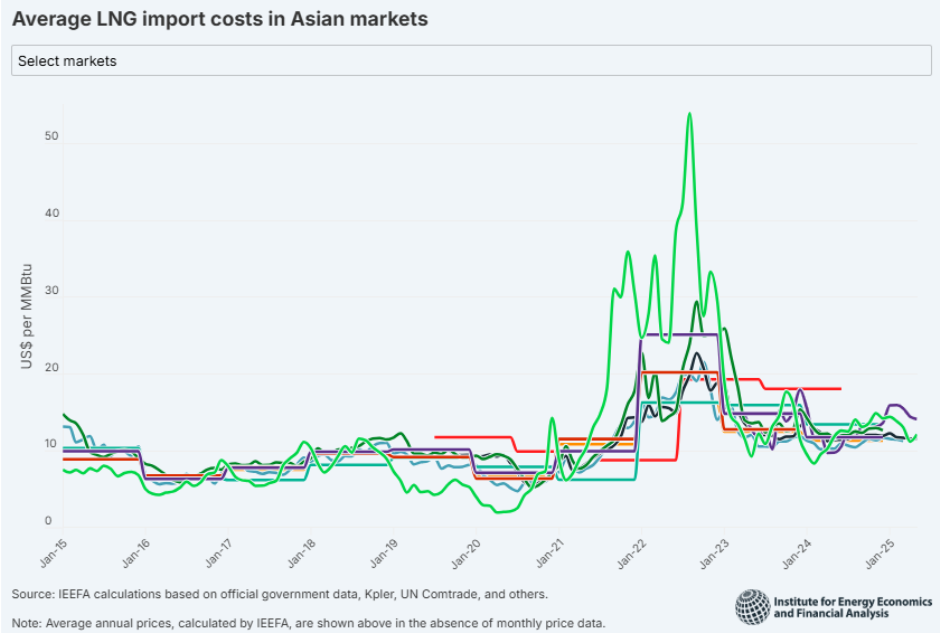

LNG import spending nearly doubles since 2015

The 14 surveyed markets, excluding Hong Kong, Indonesia, and Vietnam, spent USD 177.6 billion on LNG imports in 2023. This is nearly twice the amount spent in 2015. The shift from low cost domestic gas to higher priced LNG is creating affordability risks for industries and raising exposure to global commodity volatility.

US LNG exports fall sharply across Asia

Asia’s LNG imports were down 6 percent through October 2025. Imports from the United States fell in China, Japan, South Korea, Taiwan, and Thailand. China halted US LNG imports entirely in March 2025. These trends show that pricing continues to dictate LNG flows more than political pressure.

China accounts for most of Asia’s gas demand growth

China is responsible for more than 90 percent of Asia’s total gas demand increase since 2015. However, domestic production growth, rising pipeline imports from Russia and Central Asia, geopolitical tensions, and rapid adoption of clean alternatives may limit China’s future LNG requirements.

Natural gas demand in Asia

Asia’s natural gas consumption grew 35 percent between 2015 and 2023. China more than doubled its gas use during this period, while India, South Korea, and Taiwan recorded growth of more than 30 percent. Five countries saw combined demand falls of 31.3 bcm, led by Japan.

Sectoral demand patterns differ sharply across markets. More than half of gas consumption goes to power generation in Japan, Taiwan, Hong Kong, Singapore, Thailand, the Philippines, Vietnam, and Bangladesh. By contrast, China, India, Indonesia, and Malaysia consume 40 to 65 percent of their gas in industrial segments.

Residential and commercial consumption remains limited in countries without large pipeline networks. Transport sector demand is significant only in China and India, driven by LNG trucking in China and compressed natural gas adoption in India.

Natural gas production in Asia

Domestic gas production is falling in most markets. Declines are driven by field depletion, higher extraction costs, limited new finds, and the retreat of global oil and gas majors. China is a major exception, posting strong growth due to policy support and rapid development of unconventional gas. China produced 246.4 bcm in 2024, surpassing its 2030 target years ahead of schedule.

Southeast Asian countries are planning upstream investments that could reach more than USD 30 billion by 2027. However, new offshore projects may require prices above USD 6 to USD 7.5 per MMBtu to break even, and reliance on carbon capture technologies would add further cost burdens.

Pipeline trade is also shaping gas dynamics. China, Hong Kong, Singapore, and Thailand import pipeline gas, while Malaysia and Indonesia export pipeline volumes to Singapore. Declining pipeline supply from Myanmar could raise Thailand’s LNG needs.

LNG imports and pricing trends

From 2015 to 2024, Australia was the largest LNG supplier to Asian markets, followed by Qatar, Malaysia, the United States, and Russia. Qatar still dominates sales to South Asia due to cost advantages but has lost share in Northeast Asia.

The share of US LNG in Asia has fallen sharply in 2025. China stopped purchases entirely, and imports have also declined in Japan, South Korea, Taiwan, and Thailand. Russia’s share remains stable at about 5 percent, with China becoming the largest buyer of Russian LNG.

LNG import bills surged to USD 177.6 billion in 2023 across surveyed markets. Average prices paid vary due to contract structures, switching ability, and domestic alternatives. Thailand paid an average of USD 25 per MMBtu during the 2022 price spike, while China paid among the lowest prices due to reduced demand and its ability to resell cargoes.

Risks to future gas and LNG demand

The move from low cost domestic gas to expensive LNG threatens industrial competitiveness and raises investment risks for new LNG based infrastructure. Markets face higher fuel input costs, vulnerability to supply disruptions, and exposure to global price swings. These risks could slow future demand growth, especially in fertilizer production, petrochemicals, and energy intensive manufacturing.

Impact of lower LNG prices

Lower LNG prices could offer near term relief for importers, but structural market risks remain. Pipeline growth in China, domestic production expansion, and rapid adoption of renewable alternatives may limit the region’s ability to absorb additional LNG volumes even if prices fall.

Baburajan Kizhakedath