The global low-emissions hydrogen sector faces a more uncertain near-term outlook as project delays, slower investment decisions, and regulatory challenges reduce the pace of deployment across major markets, according to the latest International Energy Agency (IEA) assessment.

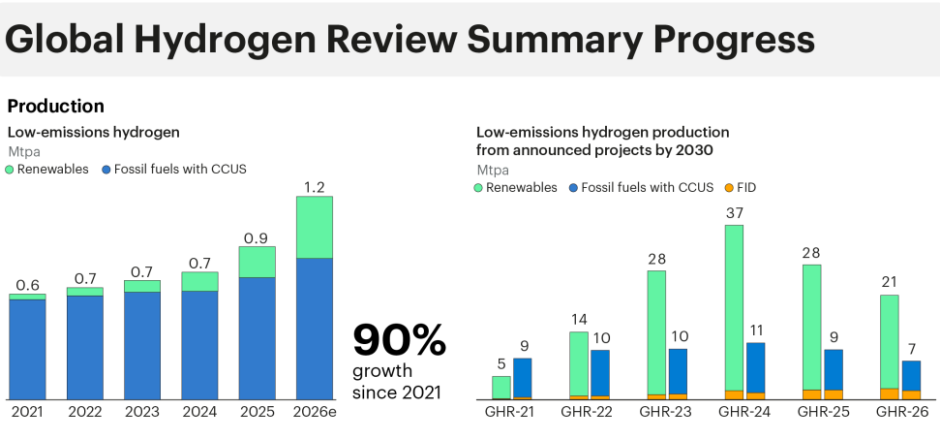

The IEA said the pipeline of announced low-emissions hydrogen production projects has fallen to 27 million tonnes (Mt) by 2030, primarily because of project cancellations and delays extending beyond 2030. Since the Global Hydrogen Review 2025 (GHR-25), only 300 kilotonnes per annum (ktpa) of additional production capacity has reached final investment decision (FID), highlighting slower investment momentum during 2025.

The agency noted that committed projects and those with strong potential to be operational by 2030 have dropped significantly from 10 Mt identified in GHR-25 to just over 6 Mt, mainly due to postponed investment decisions. Around 80 percent of this production is aimed at chemicals manufacturing, refining operations, and low-emissions fuel production, sectors where hydrogen could rapidly support energy diversification strategies, IEA report said.

The report also warns that 22 Mt of potential hydrogen production capacity in announced projects could lose any realistic chance of entering operation before 2030 if investment decisions are not taken by early 2027. Approximately two-thirds of this at-risk capacity is concentrated in Europe, North America, and Latin America.

China Remains Key Driver Despite Signs of Market Consolidation

China continues to dominate global hydrogen deployment despite emerging signs of slower growth. Global installed electrolysis capacity doubled in 2025 to exceed 4 GW, with China accounting for nearly three-quarters of new installations.

The IEA said low technology costs and experience with large-scale hydrogen projects have supported rapid expansion. However, surplus manufacturing capacity and intense domestic competition are creating market consolidation pressures. New final investment decisions for hydrogen production projects also declined for the first time in 2025.

To sustain growth, Chinese electrolyser manufacturers are increasingly targeting overseas markets. Since the second half of 2025, the Chinese government has introduced additional support mechanisms designed to expand hydrogen use into new sectors and reduce dependence on fossil fuel imports, measures expected to stimulate fresh investment activity in the coming years.

Europe Prepares for First Large-Scale Projects in 2026

Europe is expected to see its first large-scale low-emissions hydrogen projects begin operations in 2026, supported by national and European Union initiatives. Progress has been aided by the implementation of the EU Renewable Energy Directive and targets for Renewable Fuels of Non-Biological Origin (RFNBO) in transportation.

However, the IEA noted that the transposition of these regulations into national legislation has progressed slowly, while uncertainty surrounding other key regulatory frameworks continues to delay investment decisions and large-scale deployment.

North America and India Face Regulatory and Market Risks

The outlook for other major hydrogen markets remains mixed. In North America, several large carbon capture, utilisation and storage (CCUS)-based hydrogen projects have reached final investment decision. Nevertheless, most projects under development are focused on export markets, making their financial viability dependent on growing overseas demand for low-emissions hydrogen products.

Currently, such demand is largely supported by policy mechanisms in Japan and the European Union, creating additional uncertainty for developers as market conditions evolve.

In India, hydrogen development has gained momentum through tenders issued by the Solar Energy Corporation of India (SECI) and procurement initiatives from refineries, leading to multiple offtake agreements. However, the IEA cautioned that the success of these projects will largely depend on the availability and clarity of future government incentive programmes, which remain uncertain.

Policy Clarity Critical for Hydrogen Growth

The IEA concludes that while global interest in low-emissions hydrogen remains strong, investment decisions, regulatory certainty, and policy implementation will determine whether the industry can move beyond the current pipeline of 27 Mt and unlock the substantial 22 Mt of projects currently at risk. Without faster action, many projects may miss the opportunity to contribute meaningfully to global decarbonisation and energy security goals before 2030.

BABURAJAN KIZHAKEDATH