The latest Short-Term Energy Outlook from the U.S. Energy Information Administration shows that the closure of the Strait of Hormuz and related production outages are driving a broad-based disruption across global oil, gas, and power markets, with ripple effects expected to last into 2027.

According to EIA Administrator Tristan Abbey, the agency’s forecasts depend on three unprecedented variables: how long the Strait remains closed, the scale of production shut-ins, and the uncertain timeline for reopening and restoring flows. The EIA warns that even after reopening, full normalization could take months, keeping fuel prices elevated in the near term.

Oil production has taken a significant hit as restricted flows through the Strait have caused storage to fill rapidly in export-dependent countries such as Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain. The EIA estimates that these producers collectively shut in 7.5 million barrels per day of crude oil output in March, with outages rising to 9.1 million barrels per day in April. Assuming the conflict does not extend beyond April and maritime traffic gradually resumes, production shut-ins are expected to ease to 6.7 million barrels per day in May and return close to pre-conflict levels by late 2026.

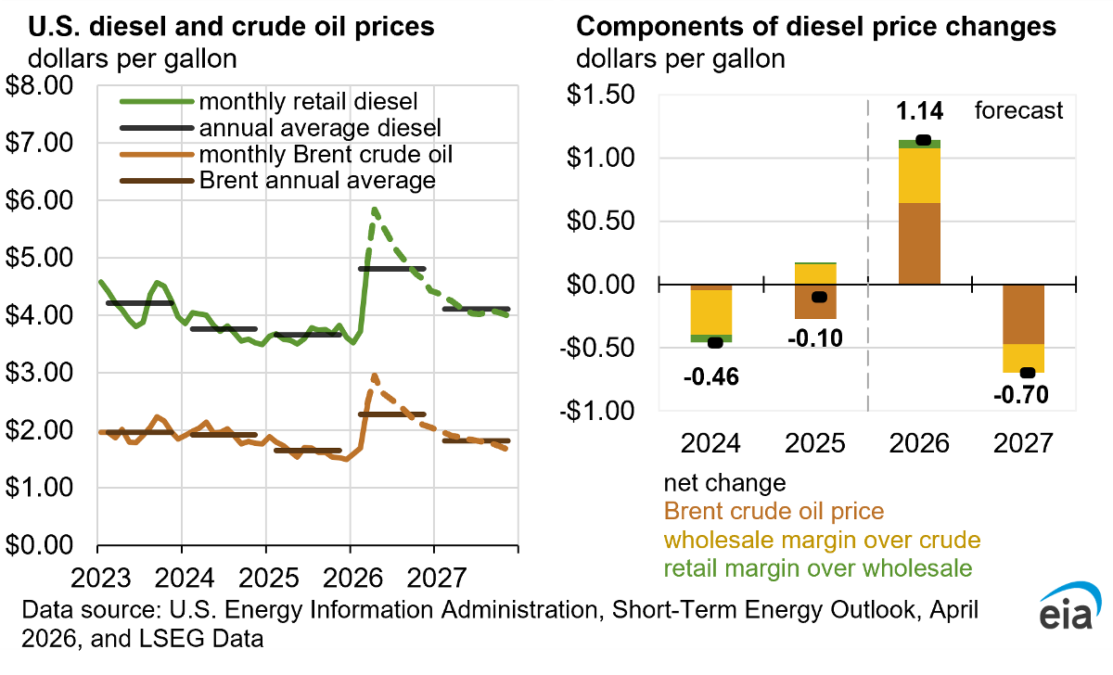

Crude oil prices have surged in response. Brent crude averaged $103 per barrel in March and is forecast to peak at $115 per barrel in the second quarter of 2026 before declining as supply disruptions ease. However, the EIA maintains a persistent risk premium in its outlook, with Brent prices expected to fall below $90 per barrel in the fourth quarter of 2026 and average $76 per barrel in 2027. The Brent-West Texas Intermediate spread widened to $12 per barrel in March and is projected to peak at $15 per barrel in April, reflecting higher shipping costs and stronger exposure of Brent-linked markets to Middle East supply disruptions.

Rising crude prices are translating directly into higher fuel costs. Retail gasoline prices are expected to peak at close to $4.30 per gallon in April and average more than $3.70 per gallon this year. Diesel prices remain under sharper pressure due to tight global supply and low U.S. inventories, peaking above $5.80 per gallon and averaging $4.80 per gallon in 2026.

The disruption is also tightening global liquefied natural gas markets. Reduced LNG flows through the Strait of Hormuz have widened the spread between the U.S. Henry Hub benchmark and European and Asian import prices. U.S. LNG export facilities are already operating near peak capacity, shipping nearly 18 billion cubic feet per day in March, close to the record set in December 2025. With utilization rates high, the ability to increase exports is limited to operational adjustments such as deferred maintenance, new project ramp-ups, and recently approved export authorizations.

Natural gas inventories in the United States remain relatively stable despite global tightness. Storage levels ended the November to March withdrawal season at just over 1,900 billion cubic feet, about 3 percent above the five-year average. Strong domestic production and limited export flexibility are expected to push inventories higher, with storage projected to reach 4,015 billion cubic feet by October, around 6 percent above the five-year average.

Electricity demand is also rising, particularly in the commercial sector. Total U.S. electricity consumption is expected to increase during the summer months of June to September, with combined residential and commercial demand growing by 3 percent compared to last summer due to higher cooling needs. Over the longer term, commercial demand is forecast to accelerate further, reaching 6 percent growth by summer 2027, significantly outpacing the residential sector’s 1 percent growth.

The EIA’s outlook underscores the central role of the Strait of Hormuz as a critical chokepoint for global energy markets. Even under assumptions of a short-lived disruption, the combined impact of production outages, constrained LNG flows, and elevated fuel demand is expected to sustain price volatility and reshape global energy balances through 2026 and beyond.

BABURAJAN KIZHAKEDATH