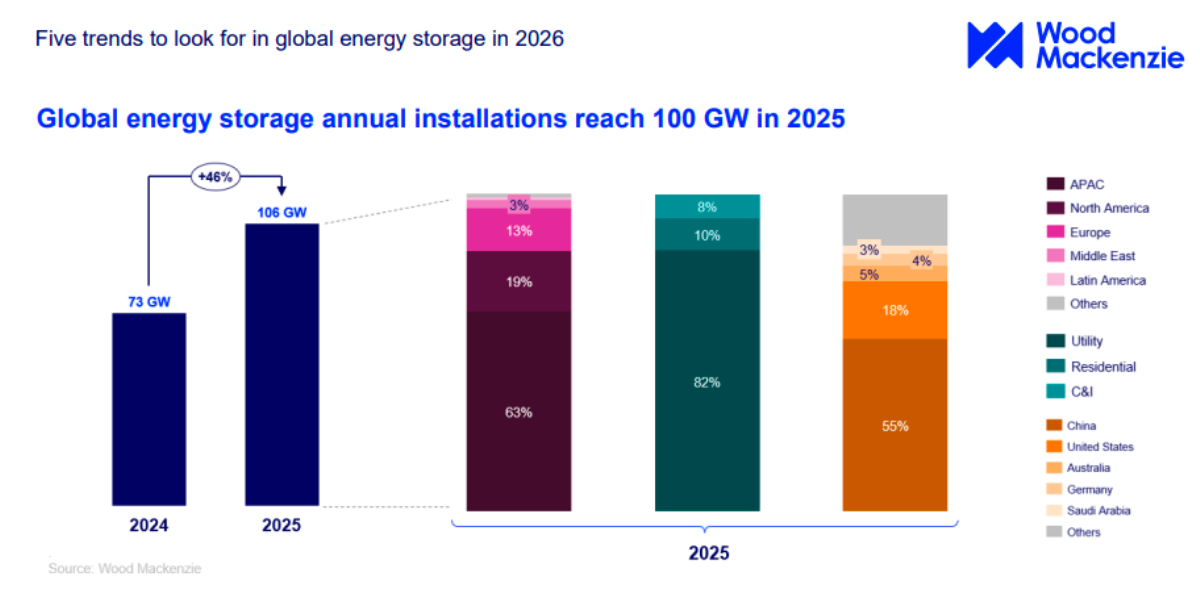

The global energy storage market is entering 2026 with strong momentum following a record-breaking 2025, when installations surpassed 100 GW for the first time. Despite significant policy shifts in key markets such as China and the United States, growth continues across regions, driven by technological advancements, cost reductions, and new applications. Wood Mackenzie’s latest analysis highlights regional trends shaping the energy storage landscape in the coming year.

United States: Short-Term Slowdown Before Long-Term Recovery

The US energy storage market faces a temporary dip in growth in 2026–2027 due to the impact of 2024 tariff changes and ongoing supply chain restructuring that restrict access to Chinese modules. Despite these constraints, the market is expected to recover by 2028 as demand for grid flexibility and renewable integration rises. Federal tax incentives continue to support installations, but developers must navigate supply chain challenges to meet growing energy storage needs.

China: Maintaining Global Leadership Amid Policy Changes

China remains a global leader in energy storage capacity growth even as the government removes the mandate to pair storage with new renewable projects. While near-term expectations are moderated, long-duration storage will continue to balance the expanding wind and solar capacity. Chinese manufacturers are increasingly targeting international markets, leveraging rising cell manufacturing capacity to stay competitive as the US market becomes less accessible.

Europe: Surging Growth Driven by Policy and Price Volatility

Europe’s energy storage market experienced a 160 percent surge in 2025, exceeding 100 GW when pumped hydro is included. Falling battery system costs, supportive government policies, and increased electricity price volatility are driving this growth. Utility-scale projects dominated installations, led by the UK with 1.8 GW deployed, while Germany remained the leader in distributed storage. Chinese manufacturers, who captured 80 percent of the residential market, are integrating smart home energy management solutions, challenging European brands beyond hardware pricing.

Latin America: Emerging Opportunities Across the Region

Growth in Latin America continued in 2025 but at a slower pace, with Chile surpassing its 2024 installation levels by 10 percent. Chile’s new remuneration mechanisms for ancillary services are expected to further stimulate the market in 2026. Mexico announced 1.3 GW of new storage capacity by the end of 2025, with more projects expected. Argentina, following the success of its latest tender, is planning additional capacity focused on grid stability. Brazil’s national storage tender faced delays but is now scheduled for early 2026, while Colombia’s upcoming regulations are expected to boost market development. Utility-scale deployments remain dominant, though Mexico leads the commercial and industrial storage segment.

Outlook: Regional Diversity Driving Global Market Growth

As energy storage markets mature, regional dynamics are becoming increasingly important. While policy and supply chain shifts affect established markets like China and the US, Europe, the Middle East, and Latin America are witnessing accelerating growth supported by government-led tenders, cost reductions, and technological innovation. Globally, long-term storage demand, evolving applications, and competitive manufacturing are expected to drive the next decade of growth in the energy storage sector.

BABURAJAN KIZHAKEDATH