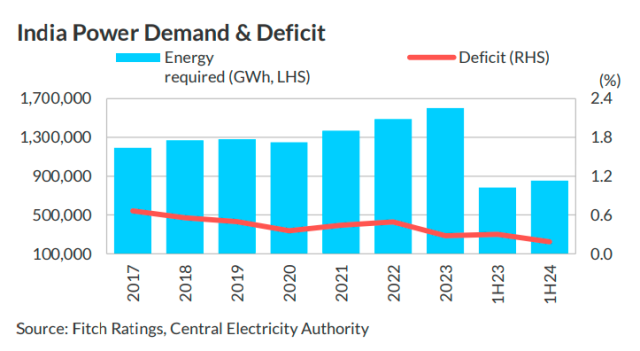

Fitch Ratings has projected an 8 percent rise in India’s power demand for 2024, slightly up from 7.6 percent growth in 2023.

This comes on the back of an 8.4 percent increase in demand during the first seven months of 2024. The boost in demand is expected to be driven by India’s industrial growth and robust economic activity, despite a moderation in the spike associated with the extreme summer heatwave from May to July.

Thermal power plants, which play a significant role in India’s power generation, saw an average plant load factor (PLF) of 72 percent in the first seven months of 2024. However, Fitch expects the PLF to stabilize at 68 percent for the remainder of the year. Despite rising demand, India’s power deficit remained minimal at less than 0.2 percent during the first half of 2024, the lowest in seven years, aided by improved coal supply and strategic capacity additions.

Renewable Energy Set for Major Growth

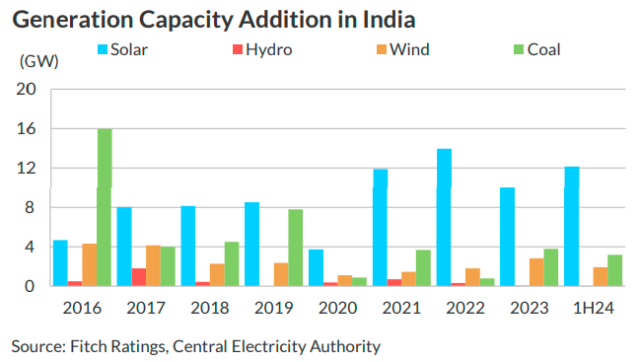

India’s renewable energy sector is poised for substantial growth, with new project auctions reaching around 70GW in FY24, more than tripling the 20GW auctioned in FY23. Solar energy dominated these auctions, contributing 48 percent of the new capacity, followed by wind energy at 9 percent and wind-solar hybrids (WSH) at 20 percent. Fitch expects the economic landscape, marked by stable interest rates and decreasing equipment prices, to support continued capacity expansion in the next two to three years.

In 2024, solar energy is anticipated to remain the leading contributor to renewable capacity, adding 12GW out of the 14GW of renewable energy installed in the first half of 2024. Wind energy, particularly in hybrid formats that include storage solutions, is also expected to see growth, spurred by government initiatives aimed at mitigating the intermittency challenges of standalone wind projects.

Thermal Power to Remain Key to India’s Energy Mix

While renewable energy is rapidly growing, thermal power is expected to maintain a significant role in India’s energy mix. Fitch forecasts that India will add 5-6GW of thermal power capacity annually in the medium term, compared to the average of 3GW per year between 2020 and 2023. By 2032, India’s thermal power capacity is expected to reach 283GW, up from 243GW in June 2024.

Although thermal power only represents 55 percent of India’s total power capacity, it accounted for 75 percent of the electricity generated in 2023. Fitch expects thermal power to remain vital until advancements in energy storage technology become widespread. Regulatory policies supporting the energy storage sector will be critical in shaping the future of India’s power landscape.

India on Track to Meet Renewable Energy Goals

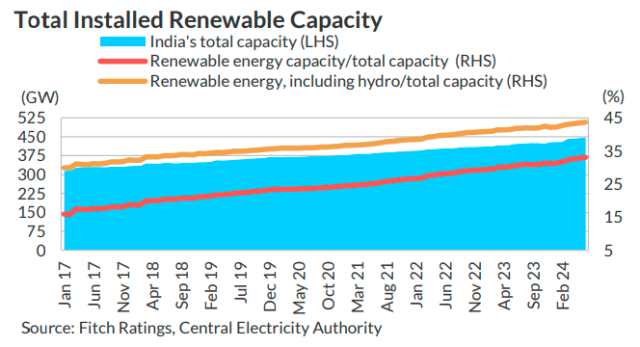

The Indian government remains committed to achieving its ambitious target of 500GW of renewable energy capacity by 2030. As of June 2024, the country had reached 194GW, up from 177GW in 2023. Key policy initiatives, such as the Green Energy Open Access Policy amendment, the National Wind-Solar Hybrid Policy, and financial support for distribution companies (discoms), have provided the necessary framework to accelerate renewable growth.

India’s renewable sector is experiencing rapid expansion, with approximately 14GW of new capacity added in the first half of 2024, driven primarily by solar energy. Fitch anticipates that renewable capacity additions in 2024 will surpass those in previous years, supported by a surge in project tenders, favorable government policies, and decreasing equipment costs.

India’s renewable energy sector is set for significant expansion in 2024, with an expected boost in capacity additions surpassing the 13GW and 16GW added in 2021 and 2022, respectively. In the first half of 2024 alone, India added approximately 14GW of renewable energy capacity, with solar contributing 12GW, up from 9GW during the same period in 2023. This growth is anticipated to continue, driven by an increase in renewable energy tenders, supportive government policies, stable interest rates, and lower equipment prices.

Wind Projects to Grow Under Hybrid Models

While solar projects have seen rapid growth, the Indian government is now focusing on accelerating wind power capacity, aiming for an additional 25GW by 2028. Since 2020, only 9GW of wind power has been added, but wind-solar hybrid (WSH) projects are expected to change the trajectory. WSH models, which combine wind and solar resources to offer more consistent electricity generation, represented 20 percent of renewable energy tenders in FY24, with standalone wind projects accounting for 9 percent.

The push for wind energy is further supported by the launch of India’s first large-scale offshore wind tender of 4GW in February 2024, divided into four 1GW blocks. Offshore wind projects are expected to benefit from storage solutions that mitigate the variable generation profile of wind energy. In June 2024, India’s Union Cabinet approved a Viability Gap Funding Program worth INR7 billion to support the development of 1GW of offshore wind projects, marking a crucial step toward realizing India’s wind energy ambitions.

Challenges for Standalone Wind Projects

Standalone wind projects have faced obstacles over the past few years, including land acquisition issues, right-of-way challenges, and fluctuating equipment prices. Additionally, the decline in solar equipment costs has drawn more investment away from wind projects. However, with the growing adoption of WSH models, demand for wind energy is expected to rebound. The hybrid model offers higher resource utilization by aligning peak demand with both wind and solar availability, making it a more attractive option for investors.

Recent Policy Changes to Support Growth

The Indian government has introduced several policy measures to ease bottlenecks in the renewable energy sector. A recent decision to remove licensing requirements for building transmission lines for bulk consumers, defined as those with at least 25MW for inter-state and 10MW for intra-state connections, will help streamline the process for renewable power projects. This move is expected to facilitate the growth of consumer-operated renewable power plants.

Energy Storage Tenders and Investments Surge

India is also advancing its energy storage sector, issuing over 35GW of energy storage system (ESS) tenders in 2023, including 22GW of standalone ESS without a renewable component. Among the leading players in the storage space is Greenko Energy Holdings, which is developing 7.20GW of integrated renewable energy storage projects. Adani Green Energy also plans to invest approximately USD3 billion in 5GW of pumped storage hydropower (PSH) capacity over the next five years.

India’s storage capacity is critical to balancing renewable energy generation, with the Central Electricity Authority’s National Electricity Plan forecasting a need for 61GW of storage capacity by FY30. This includes 19GW from PSP and 42GW from battery energy storage systems (BESS). As of 2023, India had 4.7GW of PSP capacity and less than 1GW of BESS, highlighting the need for significant expansion in the coming years.

Fitch Ratings anticipates that India’s average solar tariffs will remain stable over the next six to twelve months, despite fluctuations in equipment and component prices. This stability is largely due to the reinstatement of the Approved List of Models and Manufacturers (ALMM) for utility-scale solar projects, effective from April 2024. The ALMM mandates that government-backed solar power generation companies (gencos) source solar panels and components exclusively from domestic suppliers listed on the ALMM. These domestic components are generally more expensive than imports, particularly from China.

In recent years, solar tariffs have hovered around INR 2.4-2.5/kWh for FY23 and FY24, slightly higher than the INR 2.3-2.4/kWh range in FY20-FY21. This stability persisted despite a global decline in solar module prices, which was offset by India’s 40 percent customs duty on imported solar panels, even with an ALMM exemption in FY24. With the ALMM back in effect, Fitch expects the higher costs of domestic components to continue balancing out reductions in global equipment prices, keeping solar tariffs steady.

Wind Power Tariffs Remain Volatile Amidst Uncertainty in Bidding Mechanism

While solar tariffs are expected to remain stable, wind power tariffs have been more volatile. Over the past year, tariffs for wind projects have increased, with recent wind projects priced at approximately INR 3.4/kWh — a 20 percent rise from mid-2022 levels. This volatility is tied to the uncertainty surrounding the auctioning process for wind power capacity.

In February 2024, the Ministry of New and Renewable Energy (MNRE) announced it is considering reintroducing reverse auctions for wind projects to address issues of undersubscription and rising tariffs. Reverse auctions, where buyers submit bids to initiate the purchase, were halted in 2022 due to concerns over the slow pace of capacity additions. The lack of reverse auctions has contributed to rising tariffs for wind power projects.

As India continues its push towards renewable energy, particularly solar and wind power, the future of tariffs will depend on a combination of factors including government policies, domestic manufacturing costs, and the broader economic environment. With the ALMM reinstatement and potential changes to the wind project bidding process, the renewable energy landscape in India remains dynamic and poised for significant developments in the near future.