Europe’s electricity prices remain structurally linked to natural gas due to the marginal pricing system used in wholesale electricity markets, according to the Institute for Energy Economics and Financial Analysis (IEEFA).

Under this system, the highest-cost generation unit required to meet demand sets the clearing price, which means gas-fired plants continue to influence electricity prices even as their share of total generation declines.

This structural mechanism continues to shape pricing outcomes across Europe at a time when LNG investments, utility capital expenditure, and competitive positioning across the energy value chain are rapidly evolving, IEEFA’s Jonathan Bruegel said in the report.

Gas share versus price-setting influence remains structurally misaligned

Gas accounts for approximately 15 to 20 percent of EU electricity generation based on Eurostat and EU energy balance data. However, gas-fired plants continue to determine marginal electricity prices during peak demand periods and periods of low renewable output.

This structural misalignment means electricity prices remain influenced by gas even when gas is not the dominant source of generation.

Limited operating hours of gas plants drive disproportionate price impact

IEEFA analysis confirms that gas plants set electricity prices during a relatively small number of hours each year, typically during peak demand or low renewable output conditions.

Market data indicates that these price-setting periods occur during several hundred to approximately 1,500 hours annually in many European electricity markets. Despite representing a limited share of total operating hours, these periods strongly influence annual electricity price formation.

Gas and electricity price correlation remains structurally strong

European electricity prices remain closely correlated with gas benchmarks such as the Dutch TTF hub. During the 2021 to 2023 energy crisis period, gas prices ranged between approximately 20 to 30 euros per megawatt-hour during lower demand periods and reached approximately 60 to 70 euros per megawatt-hour during peak crisis conditions.

During the same period, wholesale electricity prices in Germany and Italy frequently ranged between 120 and 150 euros per megawatt-hour, while France recorded comparatively lower levels between 60 and 80 euros per megawatt-hour depending on nuclear generation availability.

These price ranges are consistent with European Commission energy data, ENTSO-E datasets, and IEEFA analysis.

Geopolitical disruption continues to shape energy market volatility

Electricity price volatility in Europe has been strongly influenced by geopolitical disruption affecting gas supply. The Russia-Ukraine conflict led to a significant reduction in Russian pipeline gas supplies and triggered a rapid shift toward liquefied natural gas imports.

This transition increased Europe’s exposure to global LNG markets and intensified price sensitivity to international supply-demand dynamics.

LNG expansion and global investment flows reshape supply structure

Europe’s gas supply structure has shifted significantly toward LNG imports following reduced pipeline gas flows, based on European Commission energy data.

QatarEnergy is expanding LNG production capacity toward approximately 126 million tonnes per year as part of its long-term expansion programme. Shell plc continues to operate a globally integrated LNG business spanning production, liquefaction, shipping, and trading activities that support supply to European markets.

TotalEnergies is expanding LNG trading operations while simultaneously investing in integrated gas-to-power and renewable energy systems. Eni is strengthening upstream gas production and LNG-linked supply contracts to support European demand.

MET Group is increasing LNG trading activity and expanding its role in European wholesale gas markets.

These developments reflect a structural increase in global LNG investment flows directed toward Europe and Asia, reinforcing integration between regional electricity markets and global gas supply chains.

Industry trend: Utilities increase exposure to flexible generation and trading

European utilities are increasingly adapting to volatility in gas-linked electricity markets by expanding portfolios that combine renewable energy, flexible generation, and trading capabilities.

ENTSO-E and European Commission data indicate that utilities are investing in flexible gas-fired generation, battery storage, and grid balancing infrastructure to manage intermittent renewable supply.

At the same time, utilities are increasing participation in energy trading markets to hedge exposure to price volatility. This reflects a broader industry shift toward integrated energy portfolios that combine generation, trading, and retail supply.

Competitive landscape: convergence between utilities and energy majors

The European energy market is experiencing increased convergence between traditional utilities and global oil and gas companies.

Companies such as RWE, Engie, and Iberdrola are expanding renewable energy capacity while maintaining flexible gas-based generation and energy trading operations to manage volatility.

At the same time, global energy majors are moving downstream into power generation and electricity markets, increasing competition across generation, trading, and supply segments. This convergence is reshaping Europe’s energy value chain into a more integrated but also more price-sensitive system.

Infrastructure investment accelerates across Europe

European countries have significantly expanded LNG infrastructure following the energy crisis period. Germany and other member states have deployed floating storage and regasification units, while additional investments have been made in LNG terminals, storage facilities, and cross-border interconnections.

European Commission energy infrastructure data confirms that these investments are aimed at improving supply diversification and energy security while increasing system flexibility.

However, this infrastructure expansion also increases long-term integration with global LNG markets, reinforcing exposure to international price volatility.

Regional electricity price divergence remains persistent

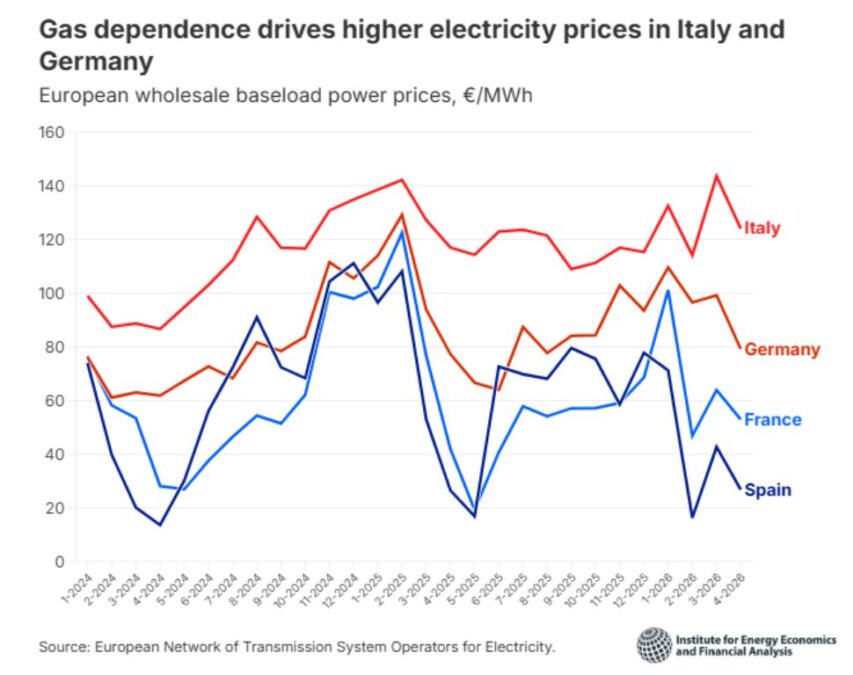

ENTSO-E and EU energy market data show persistent structural differences in electricity prices across Europe. Germany and Italy continue to record higher wholesale electricity prices due to stronger reliance on gas-fired generation. France maintains comparatively lower prices supported by nuclear energy, while Spain benefits from higher renewable penetration and targeted market mechanisms.

These differences reflect structural variations in generation mix and exposure to gas-based marginal pricing.

Market structure remains anchored in merit-order pricing

European electricity markets operate under a merit-order system in which the most expensive marginal generator required to meet demand sets wholesale prices. Gas-fired plants frequently act as marginal units during peak demand periods.

This pricing structure remains a core feature of EU electricity market design as documented by ENTSO-E and the European Commission.

Renewable energy expansion and system balancing requirement

Renewable energy generation from wind and solar has increased significantly across Europe based on Eurostat and Ember Climate data. However, due to intermittency, renewable sources do not consistently determine marginal pricing.

Gas-fired generation continues to provide balancing capacity during periods of low renewable output, maintaining its influence on electricity price formation.

Policy framework and market reform direction

European Union policy discussions include reforms such as Contracts for Difference mechanisms, capacity market adjustments, improved grid flexibility, and potential modifications to electricity pricing structures.

These measures remain under development within European Commission frameworks and are aimed at reducing volatility while supporting renewable integration.

Based on findings from the Institute for Energy Economics and Financial Analysis and supporting European energy market datasets, gas continues to function as a marginal price-setting fuel in European electricity markets.

Electricity prices remain closely correlated with gas price movements, and LNG imports have increased following the reduction of Russian pipeline supply. The existing merit-order pricing system continues to transmit global gas market volatility into European electricity prices.

FASNA SHABEER