The global electric vehicle (EV) charging infrastructure market is set for rapid growth, with total charging ports projected to rise at a 12.3 percent CAGR between 2026 and 2040, reaching 206.6 million ports worldwide, according to Wood Mackenzie’s latest EV Charging Infrastructure Forecast.

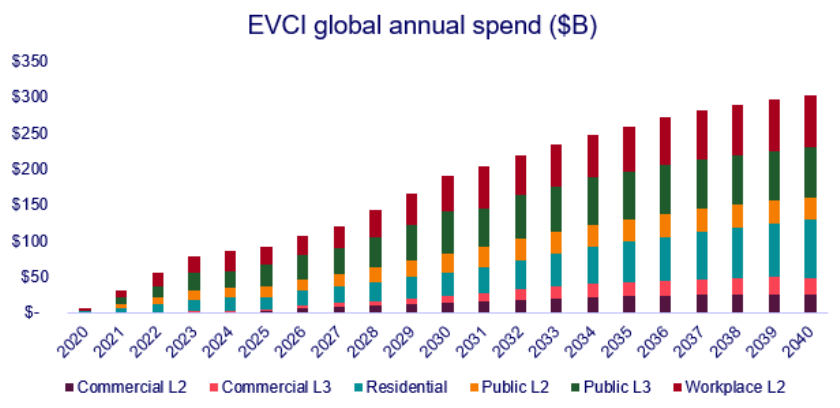

The residential EV charging market will remain the dominant segment, accounting for 133 million ports by 2040. To achieve this scale, annual global spending on EV charging infrastructure is expected to expand at an 8 percent CAGR from 2026–2040, hitting $300 billion.

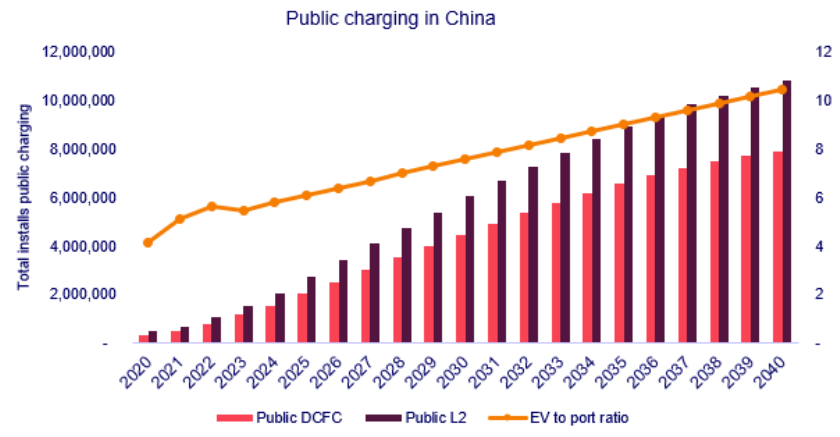

Oliver McHugh, senior EV charging research analyst at Wood Mackenzie, said: “As utilization in public charging increases and infrastructure efficiency improves, we expect the ratio of EVs to public chargers to increase from 7.5 battery electric vehicles per charger in 2025 to 14.2 in 2040.”

Emil Koenig, senior research analyst for EV charging and power and renewables at Wood Mackenzie, added: “Residential Level 2 charging dominates the global market and will comprise approximately two out of every three charging ports worldwide through 2050, offering the best balance of convenience, performance, and cost for EV owners.”

Regional Growth Outlook

Asia-Pacific: The region will drive global expansion, led by China’s dominance in public charging infrastructure. Public L3 and residential L2 segments are forecast to represent the largest CAPEX by 2040 at $54 billion and $33 billion respectively. India emerges as a key growth market, with DC fast chargers projected to rise from 14,000 today to 1.1 million by 2040, supported by strong policies and rapid EV adoption.

Americas: The US public DC fast charging (DCFC) market is expected to grow at 14 percent CAGR from 2025–2040, reaching 475,000 ports and $3.3 billion annual market value. South America is forecast to see 22 percent CAGR growth in residential charging, with residential L2 CAPEX reaching $11.2 billion by 2040.

Europe, Middle East & Africa (EMEA): Europe’s public charging network will expand at 11.3 percent CAGR through 2040, led by DC charging growth at 13.7 percent CAGR. The residential segment will reach 57 million AC chargers, while commercial charging grows at 12 percent CAGR. Saudi Arabia is expected to lead the Middle East with 29 percent CAGR growth in public DC charging, supported by ambitious government targets. The EMEA region will see $14 billion in annual public charging spend and $30 billion in residential charging investment by 2040.

Market Significance

The forecast underscores the critical role of EV charging infrastructure in supporting global electrification. With rising EV adoption, advancements in DC fast charging, residential Level 2 charging, and public charging efficiency will be key to meeting demand.

ChargePoint remains one of the largest global networks, operating well over 225,000 charging spots across more than 14 countries. In 2024, they managed around 342,000 charging ports — including about 33,000 DC fast chargers—and processed hundreds of thousands of charging sessions via partnerships with automakers like General Motors and service networks like AAA. Their R&D investments rose significantly, with USD 220.8 million in 2024 and USD 141.3 million planned for 2025, while they also introduced AI-driven platforms to enhance driver support and uptime.

Tesla’s Supercharger network leads in scale and continues expanding. As of 2025, Tesla operates roughly 7,000 stations and over 65,800 connectors across major global regions. Beyond serving its own fleet, Tesla has opened up parts of its network to non-Tesla EVs, promotes its high-powered V4 Superchargers (up to 250–350 kW) and plans extensive global expansion with 10,000+ new stations by end of 2025.

Electrify America, a VW/Siemens-backed initiative born from an emissions settlement, operates the largest open DC fast-charging network in the U.S. Their stations—spanning over 46 states plus DC—feature up to 350 kW fast charging, solar canopies, and Plug & Charge technology. They’ve committed over USD 2 billion to Zero Emission Vehicle infrastructure.

EVgo, particularly prominent in urban areas, runs more than 1,000 locations across 35 U.S. states. They’ve deployed 350 kW chargers, and have prefabricated stations that reduce installation time and cost. Strategic partnerships include GM, Uber, and a massive rollout plan of 3,250 DC fast stalls in metro markets by 2025.

BP Pulse (formerly BP Chargemaster) is accelerating growth across the UK and EU, with ultra-fast charging networks doubling in the UK in 2023. They aim for over 100,000 global charging points by 2030 and are investing approximately £1 billion (~USD 1.3 billion) in UK infrastructure over the next decade.

Shell Recharge Solutions, having integrated Ubitricity and NewMotion, commands a vast European network — hundreds of thousands of charging points. Their lamppost (street light) chargers are being widely installed, and the brand continues to invest heavily in public, workplace, and home charging ecosystems.

ABB is at the forefront of fast-charging infrastructure. Their Terra HP/DC chargers are deployed in over 85 countries. In early 2024, they partnered with Porsche for high-power charging infrastructure in North America and delivered Terra 184 units to a NEVI site in Kentucky.

Wallbox, originating from Spain, leads in residential charging innovations. Its Quasar bidirectional charger has seen over 100,000 installations in Europe and North America. Their recent acquisition of Germany’s ABL GmbH gives them additional tech and manufacturing capacity.

EVBox, part of the Engie group, had an installed base of over 190,000 charging points globally by 2020. However, sustained losses prompted Engie to announce its closure in October 2024 after years of heavy financial drains.

Other key players include BYD, a vertically integrated Chinese EV-maker providing its own charging solutions — covering depot, mobile, and public chargers — often paired with renewable energy systems, and working with Shell through joint ventures.

Tritium, an Australian DC fast charger manufacturer, has global reach and is a major supplier for highway charging stations in the U.S., Europe, and Asia. In 2025, they launched the TRI-FLEX platform at ACT Expo, enabling scalable deployments from four to 64 charge points.

Eaton and Siemens also feature in the market: Eaton’s expanding fast-charger offerings in India and strategic investments are strengthening its footprint; Siemens focuses on grid-integrated smart charging technologies and maintains agreements—like one with Shell — to advance infrastructure solutions.

India’s Charge Zone is emerging rapidly, with over 13,500 deployed chargers, especially along key highway corridors. They’ve partnered with Hyundai Motor India to expand charging network access across dealerships and facilitate intercity travel.

Baburajan Kizhakedath