India’s green hydrogen sector is gaining global attention, but project development remains slow even as the country positions itself to become a major clean energy hub, according to the Institute for Energy Economics and Financial Analysis (IEEFA).

As of August 2025, India had 158 green hydrogen projects at different stages of development. However, the pace of commissioning is still limited, with most projects yet to move beyond initial announcements.

Nearly 94 percent of the planned green hydrogen capacity is still at the announcement stage, while only 0.1 percent is under construction and 2.8 percent is operational. This highlights a widening gap between ambitious national targets and actual project execution, Charith Konda, an Energy Analyst at IEEFA, said in the report.

India’s hydrogen demand is projected to triple from 5–7 million metric tonnes per annum (MMTPA) in 2024 to 15–20 MMTPA by 2029–30, according to SBI Caps. Currently, this demand is largely met by grey hydrogen. The government aims to produce 5 MMTPA of green hydrogen by 2030, which would meet around 25–33 percent of total hydrogen demand. Industry estimates place potential green hydrogen demand between 4.08 and 6.57 MMTPA by 2030. With effective policy support, green hydrogen’s share could exceed 33 percent, driven by new demand in sectors such as steel, transportation, ammonia production, and exports.

Key Challenges Slowing Green Hydrogen Growth

Several roadblocks continue to impede the progress of India’s green hydrogen ecosystem. One of the biggest concerns is the lack of committed buyers, which has resulted in weak demand signals for producers. High production costs, inconsistent definitions of what qualifies as green hydrogen, and limited infrastructure for storage, transportation, and shared facilities further restrict scale-up efforts, Kaira Rakheja, an Energy Analyst at IEEFA, said.

Industry stakeholders also highlight the need for clarity in emissions accounting. Without a common global standard, buyers face uncertainty in verifying the carbon intensity of hydrogen, making long-term contracts harder to procure.

India’s Growing Hydrogen Demand Outlook

India’s hydrogen demand is expected to rise significantly this decade. Industry projections indicate that total hydrogen demand could reach 15 to 20 million metric tonnes per annum by 2030. With supportive policies, green hydrogen alone could account for 4.08 to 6.57 million metric tonnes per annum. This demand is expected to come from new use cases in steel production, heavy transport, chemicals, and export markets.

To unlock this potential, policy instruments such as hydrogen purchase obligations, demand aggregation models, and hydrogen hubs with shared infrastructure are being widely recommended. These measures can accelerate commercial adoption and give investors confidence to move projects from planning to construction.

Green Hydrogen as a Pillar of India’s Climate Goals

India’s green hydrogen ambitions are closely tied to its broader climate strategy. The country aims to reach net zero emissions by 2070 and increase its non fossil capacity to 50 percent of total power generation by 2030. India also targets a reduction in emissions intensity of more than 45 percent by 2030 compared to 2005 levels.

The National Green Hydrogen Mission, launched in January 2023 with an outlay of INR197 billion, is one of the central pillars supporting these goals. The mission seeks to make India a global hub for green hydrogen production, use, and exports. It targets the production of five million metric tonnes per annum of green hydrogen by 2030, supported by an estimated investment of over INR8 trillion.

Green hydrogen is also viewed as an important lever for energy security. India currently imports more than 40 percent of its primary energy needs, costing nearly INR7.9 trillion each year. By adopting green hydrogen at scale, the country could reduce fossil fuel imports by around INR1 trillion by 2030.

Meeting the mission’s production target will require significant renewable power expansion. Producing five million metric tonnes of green hydrogen will need around 125 gigawatts of additional renewable energy capacity by 2030.

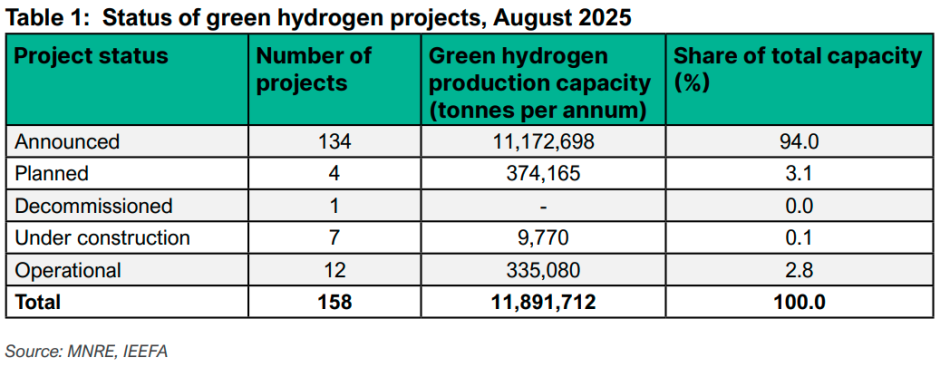

Status of Green Hydrogen Projects in India

According to the Ministry of New and Renewable Energy’s database, India’s green hydrogen industry is still at a formative stage. As of August 2025, close to 11.2 million metric tonnes per annum of green hydrogen capacity remained in the announced category, with project details yet to be finalized. Only 9,770 tonnes per annum is currently under construction, while 0.3 million metric tonnes per annum is operational.

Although the announced capacity is almost two point four times higher than the government’s target, the challenge lies in turning these commitments into real projects. Industry leaders caution that unless demand creation, infrastructure development, and regulatory clarity improve, many of these announced projects may not advance to execution.

Key Challenges Slowing India’s Green Hydrogen Adoption

India’s ambition to build a world leading green hydrogen ecosystem is gaining momentum, but the industry continues to face serious roadblocks that limit large scale adoption. High production costs, weak demand signals, policy gaps, and an underdeveloped infrastructure network remain the biggest challenges for investors and project developers. As a result, only captive projects in oil refining and projects with guaranteed offtake in fertiliser manufacturing are moving forward at a meaningful pace.

Demand Uncertainty Remains a Major Barrier

One of the most critical issues for green hydrogen developers is securing a reliable, long term buyer. According to Bloomberg, by January 2025 only 6 percent of planned global green hydrogen capacity had an identified buyer. This means nearly 212 million tonnes, or 94 percent, of capacity under planning did not have an offtaker.

This lack of anchor demand slows financial closure and delays final investment decisions. For India, where most planned projects are still in early development, the absence of committed buyers poses a significant long term risk. Potential buyers remain hesitant due to the high cost of green hydrogen and the lack of supporting infrastructure.

Although the National Green Hydrogen Mission targets production of 5 million metric tonnes per annum by 2030, it does not impose purchase obligations on major hydrogen consuming industries. While supply side incentives are available, demand creation continues to rely largely on voluntary initiatives and broad climate commitments, limiting the speed of market expansion.

High Production Costs Limit Competitiveness

Grey hydrogen, produced from natural gas, continues to dominate the market because of its lower cost. Grey hydrogen typically costs between USD1.5 and USD3 per kilogram, while green hydrogen usually ranges between USD3 and USD6 per kilogram.

Green hydrogen costs are influenced heavily by renewable energy tariffs and electrolyser prices. India benefits from some of the world’s lowest solar tariffs, around INR2.5 to INR3 per kilowatt hour, helping keep green hydrogen costs below European import prices of INR500 to INR600 per kilogram. However, green hydrogen remains more expensive than grey hydrogen in domestic industrial applications.

Electrolysers are another major cost component, priced between INR26,500 and INR106,000 per kilowatt depending on technology type and scale. This increases project capital expenditure, especially for large scale installations.

A major milestone came in June 2025 when Indian Oil Corporation conducted an auction for a 10,000 tonne per annum long term offtake agreement. The discovered price of INR397 per kilogram is among the lowest globally. However, analysts caution that this may not represent the broader national pricing landscape because the tender benefits from large scale operations and long term risk mitigation.

Infrastructure Gaps Slow Project Development

Green hydrogen’s role in decarbonising hard to abate sectors depends on supportive infrastructure such as transmission networks, electrolyser facilities, storage systems, and pipelines. India’s advantage lies in its strong electricity transmission network, which allows green hydrogen producers to rely on large renewable power flows. Transmission charge waivers for renewable energy used in hydrogen production also help lower costs.

However, several challenges persist. Transmission interconnection delays in renewable rich states are slowing commissioning timelines for new clean power capacity. Land acquisition remains difficult due to fragmented landholdings and poor land documentation.

Industrial sectors such as refining, fertilisers, and chemicals will require extensive hydrogen storage and transportation solutions, including cryogenic tanks, high pressure cylinders, and pipelines. When storage and distribution systems are built individually for each project, their costs can be three times higher than production costs. This underscores the need for shared hydrogen hubs that allow multiple producers and users to access common infrastructure.

Limited Domestic Electrolyser Manufacturing Capacity

Electrolyser manufacturing is a critical part of the green hydrogen value chain. To meet the target of producing 5 million metric tonnes per annum of green hydrogen by 2030, India will need between 60 and 100 gigawatts of electrolyser capacity. As of August 2025, only 3 gigawatts of domestic electrolyser manufacturing capacity had been awarded. This raises concerns about future import dependency, which could increase costs and slow project implementation. A rapid scale up of domestic manufacturing is essential to meet national targets and ensure long term supply chain resilience.

Baburajan Kizhakedath